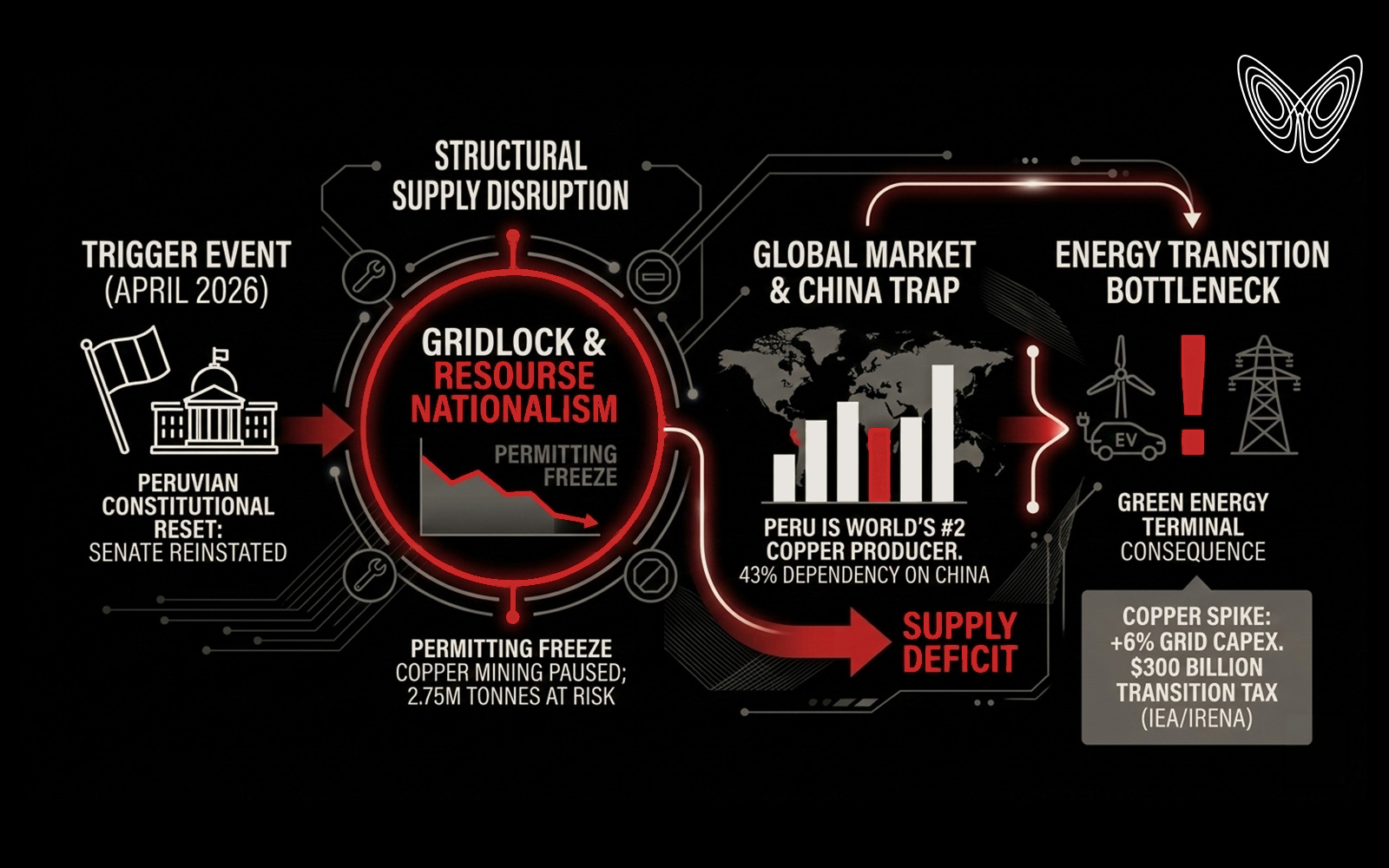

The Peruvian Constitutional Reset and the Copper Dependency Trap

There is a particular kind of blindness that afflicts sophisticated market participants. It is not ignorance. It is the comfort of a familiar story. Peru is volatile, they say. Peru has always been volatile. The mines run. The presidents change. The copper flows. They have told themselves this story so many times that they have stopped looking at whether it remains true.

The April 12, 2026 general election is not another chapter in a familiar story. It is a structural break. And the market is pricing it as noise.

What Changed

For the first time since the Fujimori constitution of 1993, Peru is reinstating a bicameral legislature. The new 60-seat Senate is not a cosmetic addition. It holds specific, non-delegable constitutional powers: exclusive ratification authority over the directors of the Central Reserve Bank, appointment power over the Constitutional Court, and the mandate to remove the Comptroller General and the Ombudsman.

These are not procedural details. They are the architectural veto points governing the legal and fiscal machinery of the state.

The election begins with 34 registered presidential candidates. The probability of any single coalition achieving a working majority across both the 130-seat Chamber of Deputies and the new Senate is statistically negligible. What the new constitutional architecture almost guarantees is a fractured Senate where ideological opposition becomes the primary legislative output. Not governance. Not reform. Not expedience. Gridlock, institutionalized.

What the Market Sees

Markets are currently treating this as standard EM election noise. The Peruvian Sol trades within its normal 12-month band, supported by robust BCRP reserves above $74 billion. The Lima Stock Exchange trades at an 18% P/E discount to its 10-year mean, which analysts attribute to "election jitters." Five-year sovereign CDS spreads sit near 75 to 80 basis points, reflecting confidence in Peru's debt-to-GDP ratio of approximately 33%.

On its face, this looks like an economy absorbing predictable turbulence.

The error is not in the data. It is in the duration assumption. The consensus expects a J-curve: disruption, then recovery. The Kuczynski transition from 2016 to 2018 tells a different story. When legislative gridlock intersects the mining sector in Peru, the lag between political trigger and production recovery is not measured in quarters. It runs 24 to 30 months.

The consensus is not wrong about the disruption. It is wrong about how long it lasts.

The Overlooked Mechanism

This is the part most analysts miss. Large-scale Peruvian mining projects are not blocked by presidential decree. They are frozen by judicial injunctions, local administrative challenges, and the slow calculus of constitutional litigation.

The new Senate's power to ratify the Constitutional Court is, in practice, the primary lever for mining disruption. A Senate-controlled court can redefine indigenous consultation rights, known as Consulta Previa, in ways that subject existing environmental impact assessments to retroactive review.

Projects like Tía María and Conga were not killed by presidents. They were killed by the legal architecture surrounding them.

The new Senate hands that architecture to whoever controls the confirmation process.

During the 2016 to 2018 period, political instability alone produced a 40% decline in mining investment as the permitting clock effectively stopped.

The Dependency That Cannot Be Rerouted

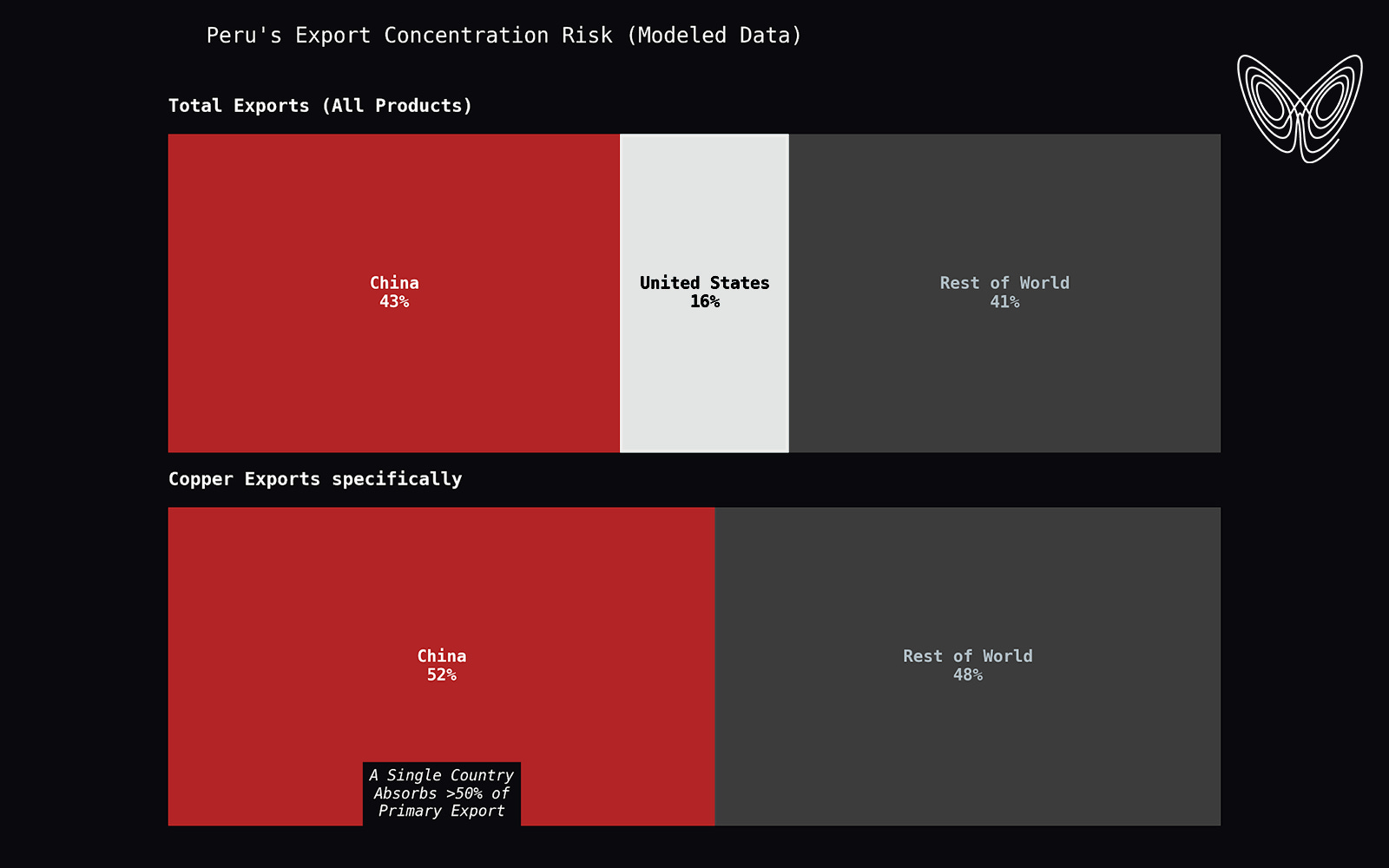

Behind that legal mechanism sits a supply chain that the global market cannot easily replace. Peru accounts for approximately 11 to 12% of global mined copper production, roughly 2.75 million metric tons annually. China absorbs 43% of all Peruvian exports, dominated by copper ores and concentrates. In 2024 alone, Peru exported $15.43 billion in copper to China.

Unlike the DRC, where Chinese equity ownership in mines creates structural leverage, Peruvian copper is fragmented and less captive. If Senate-driven regulatory nationalism begins to reshape the permitting environment, China has limited near-term alternatives. Chile supplies 23 to 27% of global copper, but is already navigating declining ore grades and water scarcity constraints that cap its production upside.

The Supply Math

The copper market is forecast to transition from a slight surplus in 2025 to a balanced state in 2026. A 15% disruption in Peruvian output — approximately 400,000 metric tons — is well within the historical range of what political strikes and permitting freezes have produced.

That 400kt disruption flips a balanced global market into immediate deficit.

Goldman Sachs research from December 2025 prices copper averaging $10,710 per tonne in H1 2026 under baseline conditions. A Peruvian supply shock pushes that toward $12,500 per tonne by year-end.

Where the Chain Terminates

The downstream arithmetic is not gentle. An EV requires 40 to 80 kilograms of copper versus 10 to 25 kilograms for an internal combustion vehicle. Onshore wind requires 3.5 tonnes per megawatt. Offshore wind requires up to 8 tonnes per megawatt. A 20% spike in copper prices adds $400 to $600 in raw material cost to an EV and raises grid infrastructure CAPEX by approximately 6%.

The G7 summit scheduled for June 15 to 17, 2026 in Évian has as a central pillar the tripling of global renewable capacity by 2030. The critical mineral supply chains those targets depend on run directly through the Andes.

IRENA estimates that between 2024 and 2030, an average of $720 billion per year must be invested in power grids and system flexibility alone to integrate new renewable capacity under the COP28 target of 11.2 TW. That is approximately $5 trillion cumulative. A sustained 20% copper price spike producing a 6% CAPEX increase adds roughly $300 billion in unanticipated cost to the global energy transition. For perspective, $300 billion is approximately equal to the entire annual GDP of Peru. The country whose constitutional calendar is creating the supply risk is also the scale reference for the damage.

The summit's ambitions and the Peruvian constitutional calendar are on a collision course that neither agenda acknowledges.

The price impact alone understates the mechanism. In the US and EU, over 3,000 GW of renewable projects are currently waiting for grid interconnection. Transformers and high-voltage sub-sea cables are copper-intensive components. When raw material costs spike, grid operators exercise what the industry calls economic curtailment:

refusing to connect new projects because the marginal infrastructure cost exceeds the project's projected return. A Peruvian supply disruption does not just make the grid more expensive. It creates a mechanical off-switch for the projects the G7 is counting on to meet its own targets.

The Candidate That Needs to Be Modeled

The consensus watches Keiko Fujimori as the establishment candidate and Antauro Humala as the radical left pole. The asymmetric position is Rafael López Aliaga. February 2026 polls place him at 10 to 14%. Polymarket prediction markets price him at 45 to 46% probability of winning, a 30-point gap that suggests informed bettors expect a rapid consolidation of the conservative base that fragmented polls are not capturing.

López Aliaga is not a resource nationalist in the traditional sense. He represents something more commercially treacherous: a pro-business protectionist who has proposed renegotiating mining royalties to fund urban security programs, a platform the fragmented Senate would likely support to expand its own fiscal base.

The market is pricing normalization. The constitutional architecture is designed to produce extraction for distribution. These are not the same outcome.

Asset Implications

Physical copper is a structural long against a supply-side deficit that permitting delays will accelerate. Southern Copper and Freeport-McMoRan carry mark-to-market exposure to Peruvian asset impairment that current valuations do not reflect.

The Sol faces capital flight pressure ahead of April 12th and deeper uncertainty around who will control BCRP board appointments under the new Senate ratification regime. Clean energy indices face margin compression as copper input costs rise against project economics that were modeled on current prices. G7 inflation swaps are not yet pricing the greenflation premium that mineral scarcity introduces into infrastructure cost curves.

But they will.

What Breaks This

Three things.

A single coalition winning 40 or more Senate seats and fast-tracking a permitting framework would change the institutional timeline. A major production surge from the DRC, specifically Tenke Fungurume or Kamoa-Kakula exceeding 2026 guidance by more than 25%, could offset a Peruvian deficit in the global balance. And a genuine technological breakthrough enabling aluminum substitution for copper in high-voltage grid wiring would alter the demand picture, though current conductivity and weight constraints make this a longer-duration possibility than the election cycle permits.

None of these is the base case.

The base case is a fragmented Senate, a stalled permitting environment, a constrained global supply curve, and a summit in Évian in June where world leaders will announce ambitions that the ground beneath them is no longer engineered to support.

The copper is still there. It is the path from ore body to cathode that is now running through an institution no one has tested in thirty years.

That is the fault line.