The Kill Switch in Budapest

There is a particular kind of risk that markets systematically underprice. Not the risk of the unexpected. The risk of the expected, arriving through a mechanism nobody modeled.

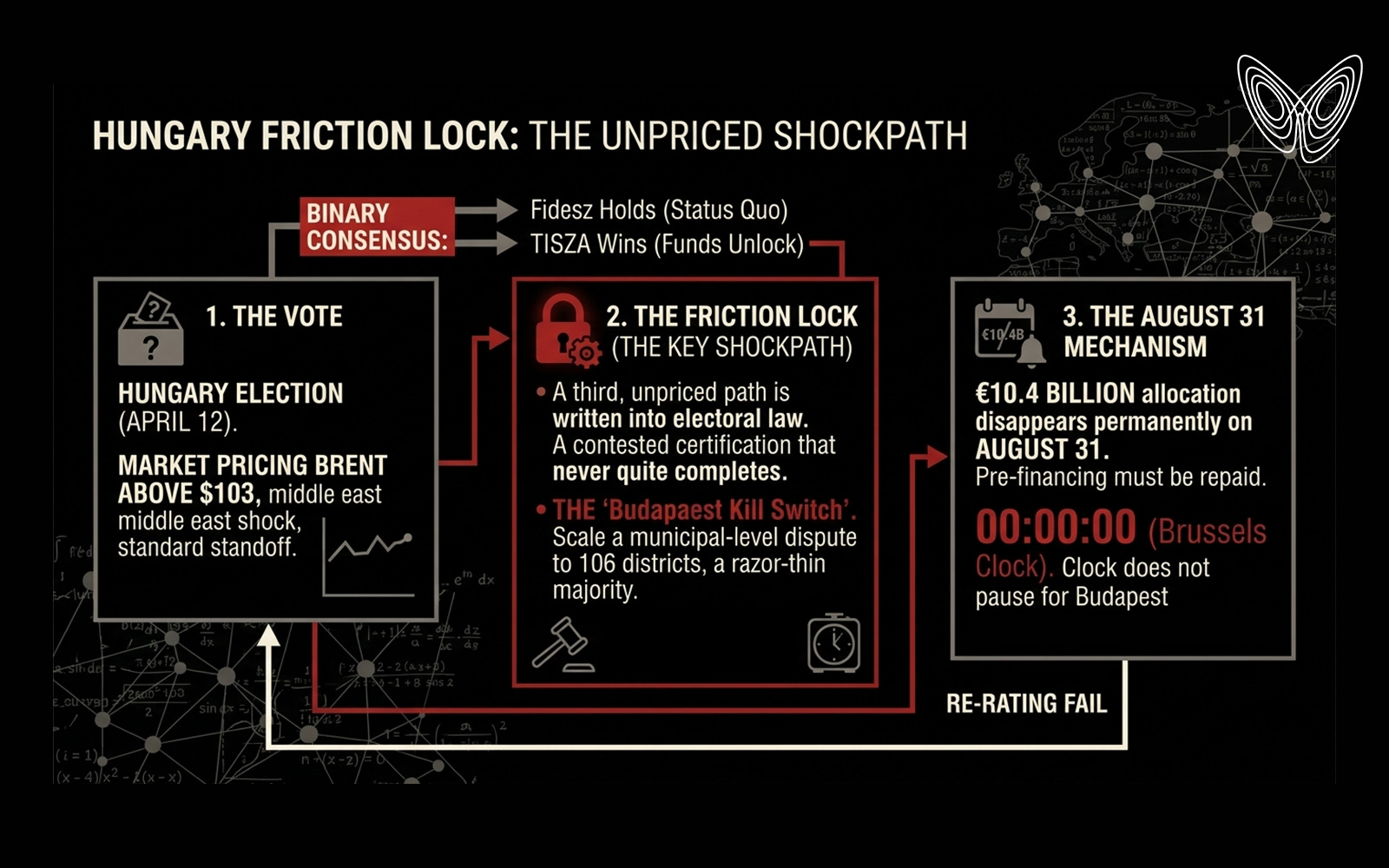

Hungary’s parliamentary election is on April 12. Independent polls show the opposition TISZA party leading Viktor Orbán’s Fidesz by 8 to 20 points. Prediction markets price a TISZA victory at roughly 70%. The political story has been covered extensively.

The financial story has not.

The market is pricing a binary outcome: Fidesz holds, status quo persists. Or TISZA wins, EU funds unlock, forint rallies. Clean signal, clear trade.

What it is not pricing is a third path. One that doesn’t require fraud. One that doesn’t require a coup. One that is written directly into Hungarian electoral law and has already been demonstrated at smaller scale.

A contested result. A certification that never quite completes. A government that cannot form while a clock in Brussels runs toward zero.

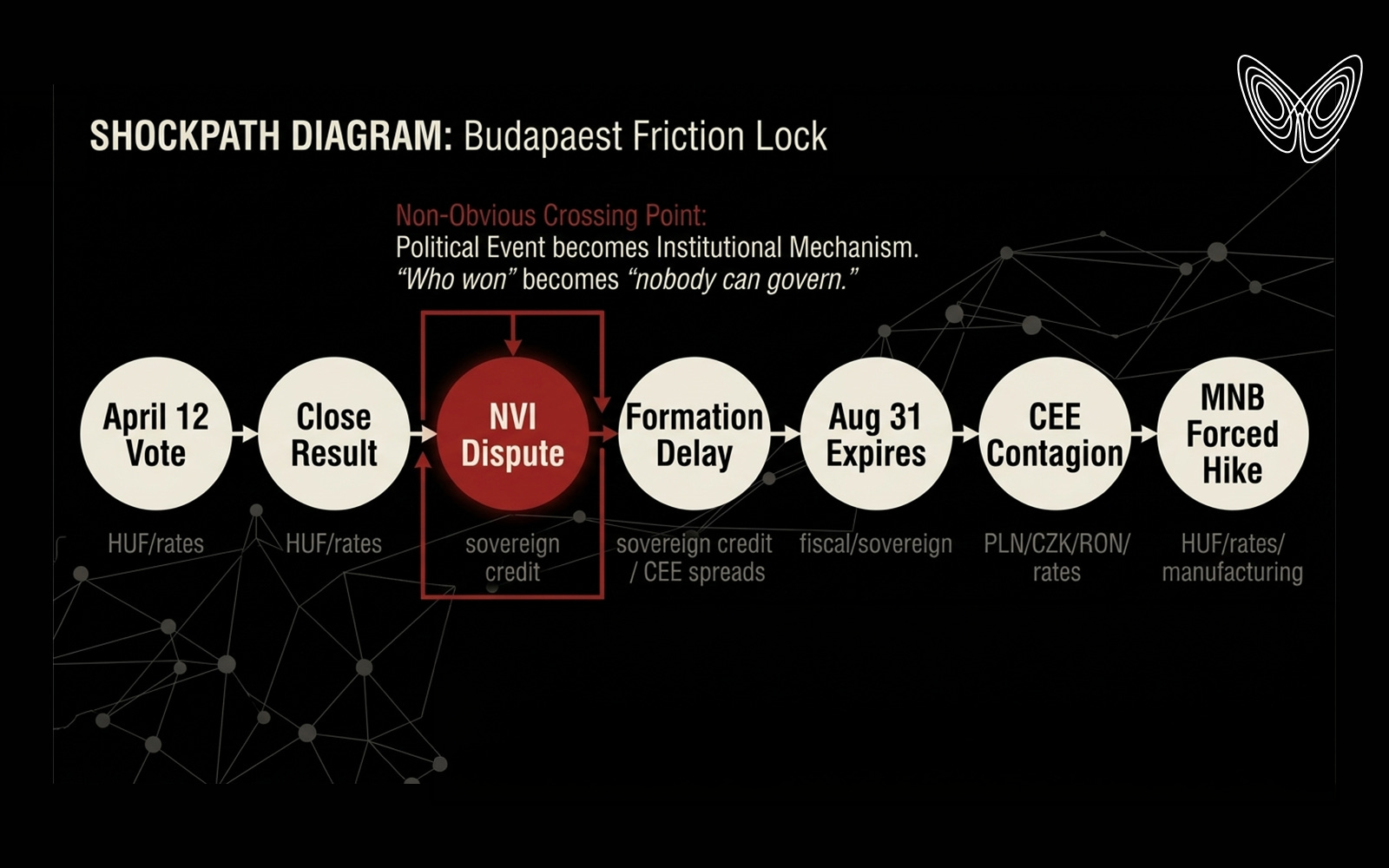

The shockpath here does not start with who wins. It starts with a procedural loophole that can prevent anyone from governing — and ends with €10.4 billion in EU funds that disappear permanently on August 31.

The Vote That Cannot Be Certified

Before a single forint moves, understand what the Hungarian National Election Office actually controls.

Under Act XXXVI of 2013, parliamentary election results are certified through a cascade of appeal windows. After preliminary results, parties have three days to file complaints in any constituency. The Kúria — Hungary’s supreme court — has three further days to rule on each. If a mandatory recount is ordered and the mathematical possibility of a result change exists, the certification deadline extends automatically. If the Kúria orders a repeated vote in a single district, that vote must be held within 30 days.

Here is the structural pivot: because Hungary’s system routes surplus and losing SMD votes into the national party-list calculation, one contested single-member district does not produce a delayed result for that seat alone. It delays finalization of all 93 proportional seats. Every list mandate — the seats that determine whether any party has a working majority — sits in legal limbo until the last contested constituency resolves.

The precedent is not theoretical. The 2024 Budapest mayoral election required a full NVB recount. The final margin: 41 votes. The process took weeks and triggered multiple appeal layers before it was done.

Now scale that to 106 districts, a razor-thin national majority, and institutions whose leadership was appointed by the parliament they are adjudicating.

The NVI president serves on the Prime Minister’s recommendation. The NVB members are appointed by a Fidesz supermajority. The Kúria president was elected over the National Judicial Council’s objections by that same supermajority. The OSCE’s 2022 observation mission found that half of filed electoral complaints were rejected on technical grounds, and that most case handling fell short of providing effective legal remedy. A full OSCE Election Observation Mission opened on February 26, 2026 — 15 experts, 200 planned short-term observers. Their presence signals the international community’s expectation that this certification will require watching.

None of this requires a smoking gun. The mechanism is the smoking gun. Delay is not a conspiracy. It is a feature.

What the Market Is Pricing

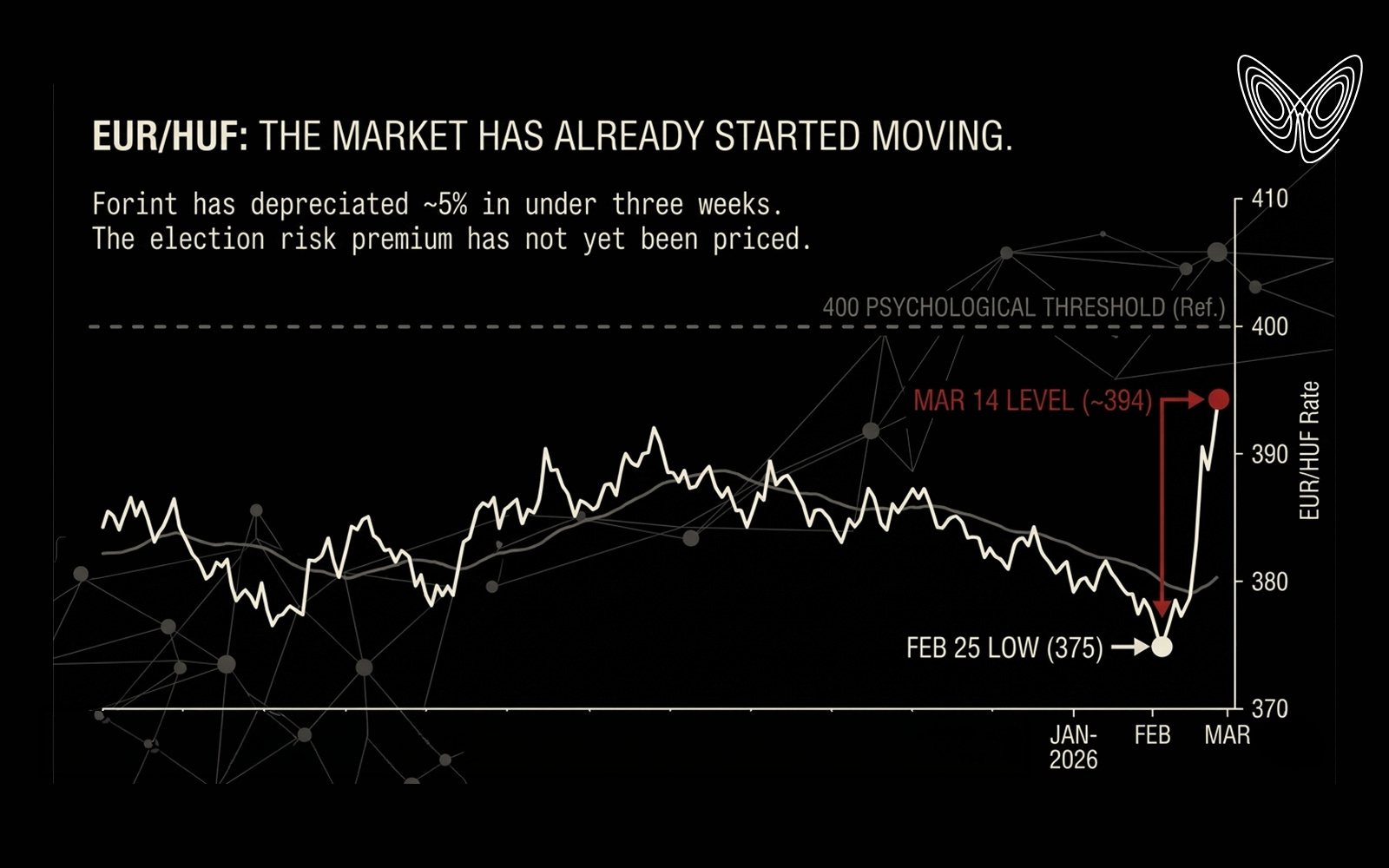

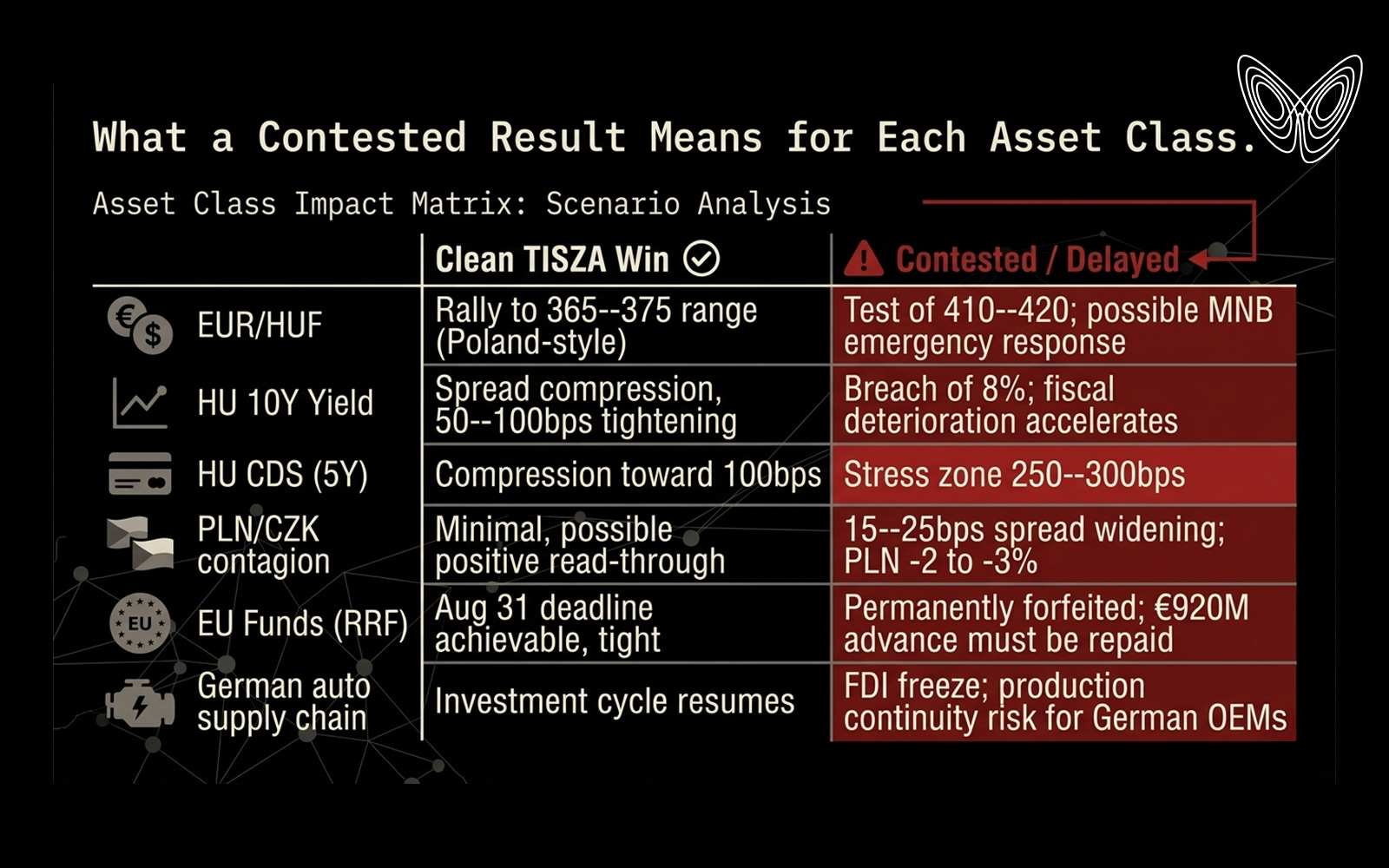

Hungarian CDS spreads are trading in the 180–220 basis point range. The forint sits at approximately EUR/HUF 394, already weakened by the Middle East oil shock, down from a 2026 low of 375 on February 25. Ten-year government bond yields have broken above 7.4%, a 90 basis-point selloff in one month, spread over German Bunds at roughly 445 basis points — second-highest in the EU.

These are elevated numbers. They are not crisis numbers. They reflect a market that has absorbed the Hormuz shock, repriced for oil above $103, and factored in the ongoing EU funds standoff with Brussels. What they do not reflect is any meaningful probability weight on a multi-month certification dispute. The implied probability in CDS pricing is consistent with a view that either outcome — Fidesz holds, or TISZA wins cleanly — resolves within a normal post-election window.

The consensus is treating this as a political binary. It is not a political binary. It is a procedural trilemma.

The third path — contested result, extended certification, government formation delayed past June — is not priced. And it is the path most compatible with the institutional architecture that exists in Budapest today.

The Magyar Nemzeti Bank cut its base rate to 6.25% on February 24, the first reduction in 18 months. January inflation had fallen to 2.1%, below target for the first time in five years. The easing cycle had finally begun.

A contested election and EUR/HUF testing 410 would end it immediately. The MNB’s October 2022 playbook — an effective overnight rate of 18%, a de facto 500 basis-point emergency tightening — is institutional memory, not ancient history. A 200 basis-point defensive hike back toward the prior 6.5% level would be the minimum response to a forint in freefall. That hike would transmit directly into the manufacturing sector’s financing costs, arriving precisely when political uncertainty is already freezing investment decisions.

The Structural Advantage That Polling Cannot Capture

The polling situation deserves its own treatment, because the divergence is analytically interesting in itself.

Independent Hungarian pollsters — Medián, Závecz Research, 21 Kutatóközpont, Publicus — show TISZA leading by 8 to 20 points among decided voters. The PolitPro weighted aggregator, which blends all firms, settles on roughly TISZA 47%, Fidesz 40%. Government-aligned pollsters — Nézőpont, Századvég — show Fidesz ahead by 5 to 10 points.

This divergence is unprecedented in Hungarian polling history. It is not a normal sampling variance. Political scientist Gábor Török described it as “unexplainable on research grounds.” The methodological dispute centers on undecided voter allocation: pro-government firms reclassify sympathetic undecideds as Fidesz voters. Independent firms do not.

But the more important variable than the polling gap is the translation problem.

Hungary’s 106 single-member constituencies elect via first-past-the-post. District boundaries were redrawn in December 2024 under Act LXXIX, removing two seats from Budapest and adding two to more Fidesz-friendly Pest County, affecting 39 of 106 constituencies. The winner-compensation mechanism routes surplus votes from winning SMD candidates back to the party list, amplifying the leading party’s proportional seat share. Roughly 373,000 diaspora voters — over 90% Fidesz — cast ballots exclusively on the party list, inflating Fidesz’s list share by approximately one percentage point regardless of the domestic result.

Political Capital’s Mandate Calculator shows that at an exact 50-50 popular vote, Fidesz wins 58 single-member districts versus 48 for TISZA — a 10-seat structural asymmetry before a single list seat is allocated. Publicus estimates TISZA needs a 5 to 6 point popular vote lead for a parliamentary majority. Some analysts place the threshold even higher.

TISZA is leading in the polls by more than enough. TISZA is leading in the polls by potentially not enough. Those are two entirely different statements about the same data.

The August 31 Mechanism

This is where the shockpath crosses from a political story into a financial one with a fixed, immovable deadline.

Hungary’s Recovery and Resilience Facility allocation is €10.4 billion — €5.8 billion in grants and €4.6 billion in loans. Of this, approximately €920 million in prefinancing has been disbursed. The remaining €9.5 billion is blocked pending 27 “super-milestones” related to judicial independence and anti-corruption that Hungary has not met in three years of negotiations. The broader frozen EU funds picture, including cohesion funds suspended under the Conditionality Regulation, brings the total at-risk figure above €18 billion.

The hard constraint is August 31, 2026. Under the RRF regulation, if Hungary does not meet its milestones and submit valid payment requests by that date, the entire €10.4 billion allocation is permanently forfeited. The €920 million already advanced must be repaid. There is no extension mechanism. There is no political override. The deadline is a treaty obligation, not a policy choice.

A TISZA government sworn in by mid-May would have approximately three months to satisfy conditions that Fidesz could not meet in three years. That is extremely tight but not impossible — the Polish precedent suggests Brussels moves quickly when the political will exists.

A certification dispute that delays government formation by eight weeks makes it mathematically impossible.

The Commission retains no mechanism to freeze already-released funds due to a contested election, but it has tools: the Conditionality Regulation permits new measures if rule-of-law breaches threaten the EU budget, and financial correction mechanisms allow clawback. Neither requires unanimity. Both require Commission initiative.

A government that cannot form is not a government that can unlock €10.4 billion. The clock does not pause for constitutional procedures.

The Poland Precedent — And Why It Cuts Both Ways

The nearest historical analogue is Poland’s October 15, 2023 election. The lesson is real. So is its limit.

Poland’s opposition won a decisive majority. The transition took 59 days — President Duda first tasked the incumbent Morawiecki with forming a government, which failed, before Donald Tusk was sworn in on December 13. Markets did not wait. The zloty began rallying on the Monday open, October 16. EUR/PLN moved from approximately 4.55 pre-election to 4.29 on inauguration day — a 5 to 7% appreciation over two months. Warsaw equities gained nearly 3% in the first week.

The Poland precedent is bullish for a clean TISZA victory. A 5 to 8% forint rally, significant bond spread compression, a re-rating of the EU funds probability — all plausible in that scenario.

But Poland is not Hungary, and the differences matter more than the similarities.

Poland entered the transition at A-/A2 rated, with deep, liquid capital markets, a 2.7% deficit and a clear parliamentary majority. TISZA would be inheriting BBB- with a negative outlook, 10-year yields above 7%, a two-decade backlog of institutional damage, and a June-August window to satisfy conditions that require genuine judicial independence reform. The Polish transition was delayed by constitutional procedure but never genuinely contested. The Kúria and NVB were not Tusk adversaries.

The Poland precedent also illustrates the asymmetry in play. When the transition was clean and clearly legitimate, markets priced it within days. When outcomes are contested, they do not give the same benefit of the doubt. PLN rallied on Day 1 because there was no structural ambiguity about who had won.

The consensus is not wrong that a TISZA victory is bullish. It is wrong about the probability that a TISZA victory arrives cleanly enough for markets to price it the same way.

Where the Cascade Lands

A contested certification does not stay inside Hungary’s borders. The transmission is mechanical.

Hungary’s CDS has historically Granger-caused Czech and Polish CDS — meaning Hungarian stress moves first, regional spread widening follows. During the February 2022 Russia-Ukraine shock, the forint lost 14.8% against the euro. The zloty lost 7.6%. The koruna 5.3%. The declining-beta pattern is consistent: Hungary is the epicenter, the CEE-4 trades as a basket in acute stress episodes.

Four channels carry the infection. The portfolio channel runs through Poland’s liquid currency market — investors reducing CEE exposure sell PLN first, since it is the most liquid instrument in the region, creating paradoxical contagion to the strongest sovereign. The banking channel runs through Austrian parent institutions — Erste, Raiffeisen, UniCredit — whose cross-border lending spans all four CEE countries; stress in one subsidiary triggers regional deleveraging. In Q3 2011, eurozone banks withdrew $35 billion from CEE operations in a single quarter. The fund allocation channel hits dedicated CEE/EM Europe mandates where redemptions force proportional selling across all constituents. The index channel reflects shared GBI-EM and similar benchmark membership.

During Hungary-specific political events — as opposed to global risk-off shocks — the contagion beta runs at roughly 0.3 to 0.5x for Poland and Czech Republic. At current spread levels, that translates to 15 to 25 basis points of widening in Polish and Czech sovereign spreads from a purely Hungarian certification crisis. Romania, rated BBB- with larger fiscal deficits, shows comparable sensitivity to Hungary-specific events.

This is not catastrophic contagion. It is a meaningful repricing of a risk that is currently priced at approximately zero.

What Is Actually At Stake Beyond the Forint

The automotive supply chain exposure elevates this story beyond a regional credit event.

Hungary exports $41.7 billion annually to Germany — approximately 25% of total Hungarian exports. Audi Hungaria in Győr produced 1.58 million engines and 179,710 vehicles in 2024, generating €8.6 billion in revenue from a single facility. That one plant accounts for roughly 7% of Hungary’s total exports. Mercedes-Benz Kecskemét is scaling toward 30% of European Mercedes production. BMW’s Debrecen facility — the global launch site for its next-generation electric architecture — began series production in October 2025.

CATL’s €7.3 billion gigafactory in Debrecen is targeting cell production in early 2026. BYD is constructing its first European EV factory in Szeged. The automotive sector directly accounts for 5% of Hungarian GDP and 21% of total exports.

Political disruption severe enough to freeze investment decisions or raise the cost of capital for Hungarian operations does not stay in Budapest. It arrives in Ingolstadt, Stuttgart, and Munich — in the form of supply chain uncertainty at a moment when German OEMs are already navigating the most difficult industrial transition in their history.

A multi-month constitutional crisis in Hungary is a supply chain risk event for European automotive. It is priced as neither.

What Would Break This Analysis

Two conditions would change the thesis materially.

First: a decisive, uncontestable TISZA majority. If TISZA wins by 8 or more points in the popular vote and the seat translation is clean enough that no SMD is within recount range, the certification dispute scenario collapses. The Poland playbook applies. The forint rallies before the new government is sworn in. The timeline to August 31 becomes achievable, if brutally tight.

Second: a Fidesz majority through the structural advantage. The gerrymandering works, the 5-to-6 point threshold protects Orbán’s majority despite the polling deficit, and the certification is clean because the incumbent controls the process and has nothing to contest. Status quo persists — EUR/HUF drifts back toward 385, 10-year yields stabilize, €10.4 billion is permanently forfeited in August, and the rating agencies deliver the downgrade they have been signaling since 2025. A slower, quieter version of the deterioration already in progress.

The scenario this analysis is specifically about is the middle path. A result close enough to contest. An institutional architecture designed to slow resolution. A Brussels deadline indifferent to Budapest’s constitutional calendar.

Mi Hazánk, the far-right party polling at approximately 6% — just above the 5% parliamentary threshold — is the additional variable that could produce a hung parliament with no clear governing path. That scenario is not the base case. It is the tail risk that makes the middle path more likely, not less.

The market is pricing two outcomes. There are three. The unpriced one is the worst.

The Fault Line

Poland in 2023 taught the market one lesson: when a populist incumbent loses cleanly, the transition delay is noise and the EU funds unlock is the signal.

Hungary in 2026 has the same setup but a different substrate. The institutions are captured more completely. The electoral system was reengineered more recently. The certification architecture has a documented kill switch that has already been demonstrated at municipal scale. And the Brussels deadline is not a soft target with extension mechanisms — it is a treaty obligation with a specific date and a specific consequence.

The forint at 394 is priced for uncertainty. It is not priced for a scenario where uncertainty becomes the permanent condition. Where the election produces a result that is simultaneously undeniable and uncertifiable. Where the government that needs to form cannot form quickly enough to matter.

That is not a prediction. It is a mechanism. One that exists in the law, has been used at smaller scale, and costs nothing to deploy.

The clock in Brussels does not read Hungarian electoral law. It reads the calendar.

August 31 arrives on schedule regardless of what is still being argued in Budapest.

That is the fault line. And the market has not mapped it.