The Baltic-Cairo Transmission: A Retrospective on the 2022 European Energy Shockpath

They called it a supply disruption. A cold winter that never came. A crisis managed, contained, filed away. The consensus always reaches for the simplest frame. It is easier that way. Easier than admitting what actually broke.

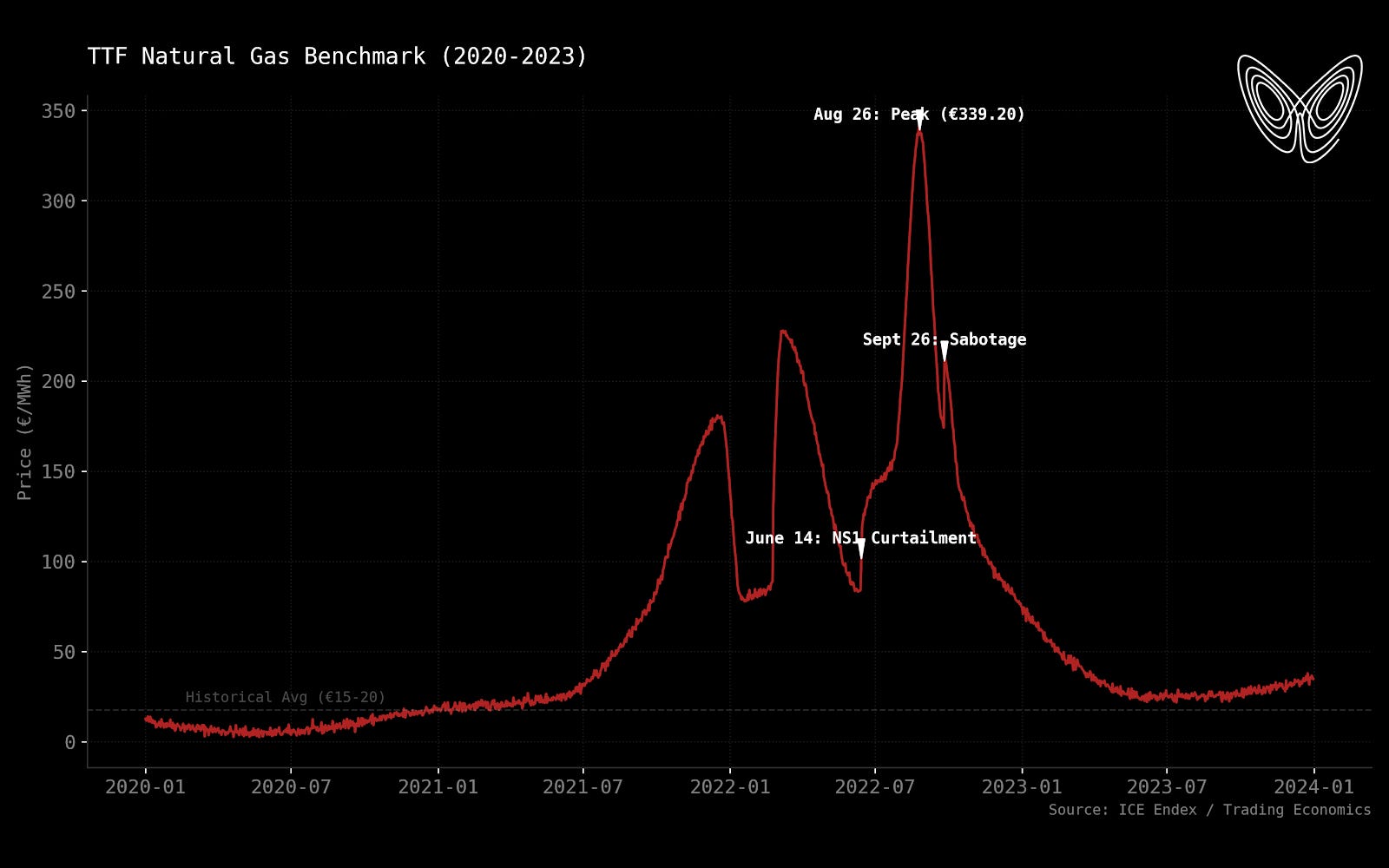

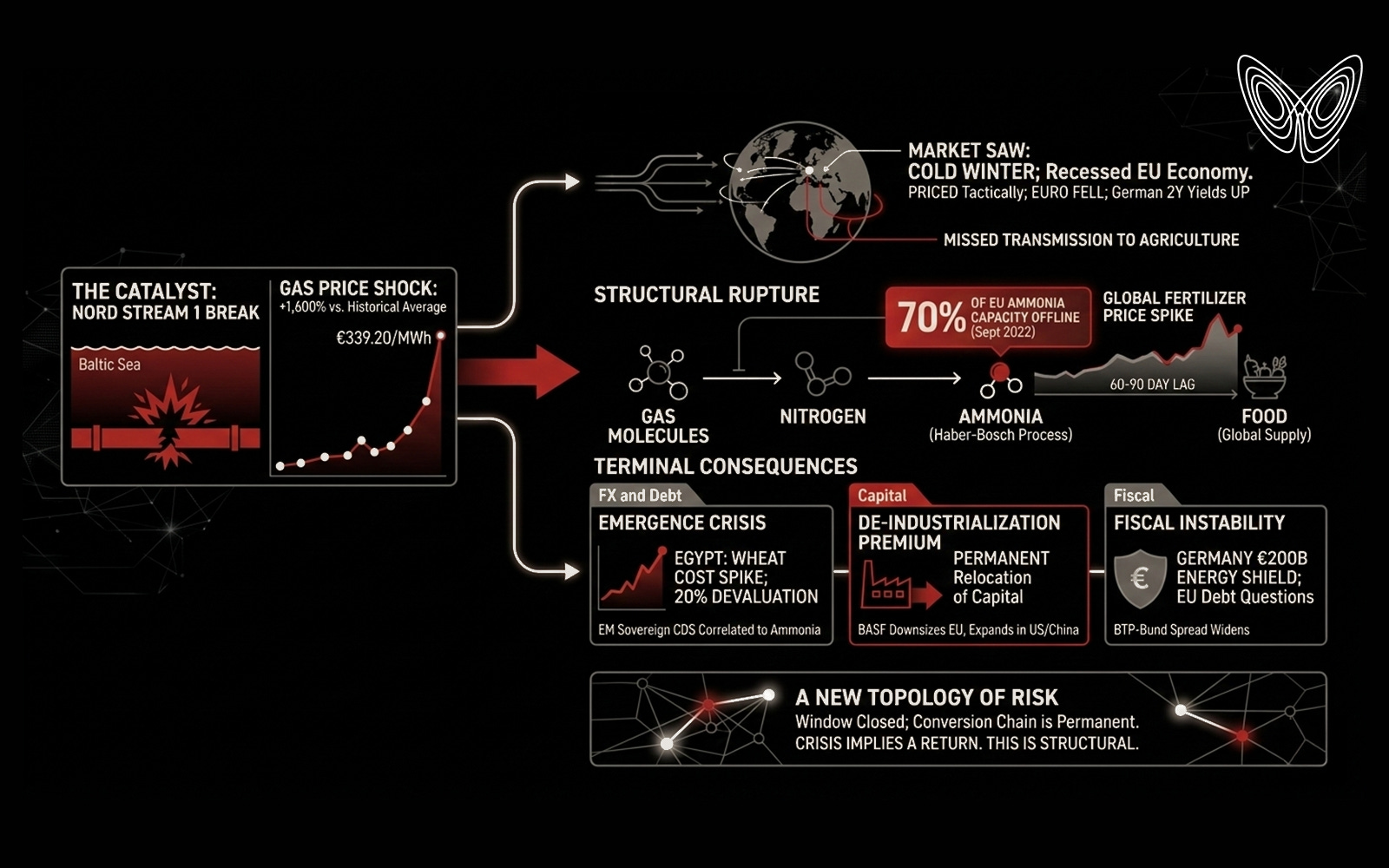

What broke in 2022 was a chain. Not a metaphor. A literal sequence: molecules from the Baltic Sea converted into nitrogen, nitrogen into ammonia, ammonia into food for eight billion people. Nord Stream 1 carried roughly 55 billion cubic meters of gas annually into Europe. Before June of that year, Germany drew 35% of its total consumption through that single corridor. Then Gazprom throttled it to 40% capacity. Then 20%. Then maintenance. Then, on September 26th, underwater explosions near Bornholm ended the matter permanently.

The TTF benchmark peaked at €339.20/MWh on August 26th. The historical average, 2010 through 2020, was €15 to €20/MWh.

A 1,600% deviation from the mean. Not a risk event. A category break.

Crisis Transmission

Markets saw a cold winter and priced accordingly. EUR/USD fell through parity on August 22nd, bottoming at 0.9535 by late September. The DAX traded down near 11,860 carrying what analysts named a "de-industrialization premium," as though the death of an industrial model deserved something so clinical. German 2-year Bund yields swung from -0.60% to 1.75% inside nine months. The ECB forced to fight inflation while recession gathered at the door.

The market correctly identified the existence of a crisis. It failed to model the transmission of that crisis through non-energy sectors. Specifically: global agriculture. Specifically: sovereign credit in the Global South.

Structural Rupture

The Haber-Bosch process. Natural gas in European ammonia production is not merely fuel. It is the feedstock. Seventy to eighty percent of variable cost. When TTF hit €339, the arithmetic turned lethal.

By late August, Yara had curtailed European ammonia capacity to 35%. CF Industries shuttered its Billingham plant, the UK's largest. BASF cut Ludwigshafen. Roughly 70% of European ammonia production was offline by September.

That is not a headline. That is a structural rupture in global nitrogen supply.

Global urea prices ran from $400 per ton in early 2021 to over $900 by mid-2022. The lag between the June curtailment and the fertilizer peak was 60 to 90 days. Inventory depletion. Spot market panic. The sequence was mechanical, and the market did not trace it.

Cairo Felt the Baltic Before Berlin Did

Egypt, the world's largest wheat importer, subsidizes bread for over 70 million people. The combined shock of the Russia-Ukraine supply disruption and the fertilizer price spike cost Egypt an estimated $1.5 billion annually in wheat imports. On October 27th, the Egyptian pound devalued from 19.7 to 24.2 against the dollar in a single session.

The FAO Food Price Index hit 159.7 in March 2022, an all-time high. Gas prices fell later in the year. Food costs did not. The 2023 harvest was already priced at 2022 fertilizer rates. Inflation does not wait for resolution.

The Relocation That Isn't Coming Back

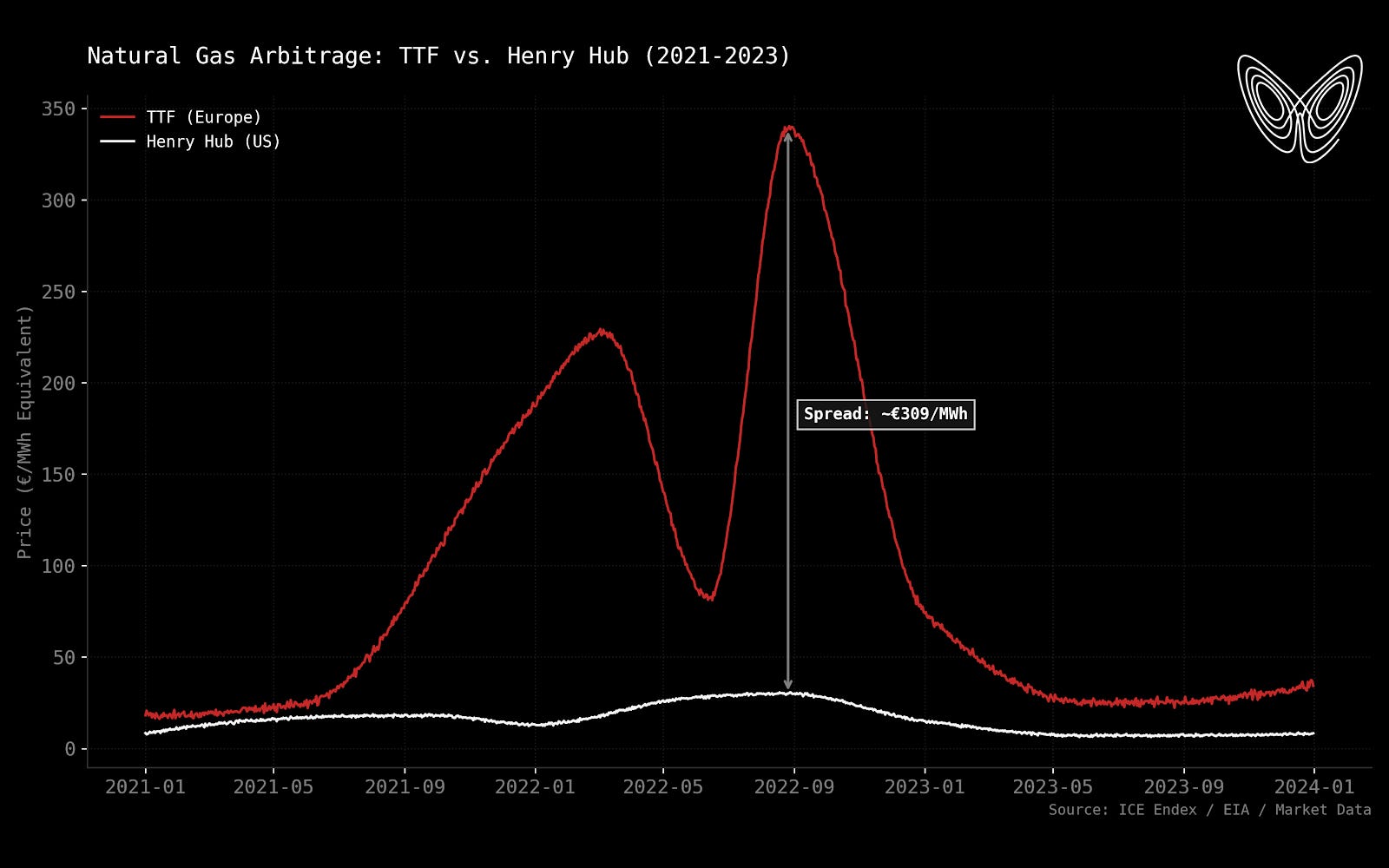

BASF CEO Martin Brudermüller announced in October 2022 a permanent downsizing of European operations. The firm accelerated a €10 billion investment in Zhanjiang, China, and expanded capacity in Louisiana, where Henry Hub gas was a fraction of TTF.

This is not a tactical adjustment. It is a permanent transfer of productive capital from one geography to another.

The structural loss to German GDP is estimated at 0.5% to 1.1% annually through 2030. Not a recession. A slow drain. The kind that doesn't make headlines until the cumulative effect becomes impossible to ignore, by which point the capital is already gone.

Germany announced a €200 billion Energy Shield on September 29th, funded through an off-budget stabilization vehicle. It suppressed the immediate social pressure. It also signaled the end of European fiscal restraint. The BTP-Bund spread widened to 250 basis points in late September as markets wondered, quietly, whether national-level bailouts could hold without EU-wide joint debt. They are still wondering.

Why 1973 Doesn't Apply

The OPEC embargo is the reflex comparison. It does not hold.

In 1973, a supply shock raised transport and heating costs. The global population was 3.9 billion. Synthetic nitrogen was not yet the backbone of caloric production.

In 2022, the population was 8 billion. Modern agriculture is a system for turning gas into calories via the Haber-Bosch process.

When oil quadrupled in 1973, you drove less. When gas rose 16x in 2022, you could not simply farm less. The inelasticity is total.

The downstream consequence is caloric instability at a scale that has no 20th-century precedent.

What This Repriced — Permanently

The shockpath from the Baltic to Cairo did not retrace when gas prices fell. Several structural correlations shifted and have not reverted.

US-based nitrogen producers like CF Industries and Nutrien are no longer valued primarily on their relationship to Henry Hub natural gas. They are now the global marginal cost setters. When TTF spikes, the entire spread flows to them as profit. The trade that the consensus missed in late 2022 — long US nitrogen, short European manufacturers — was a direct play on permanently diverged input costs. It remains open.

In emerging market sovereign credit, the fertilizer-food lag of 9 to 15 months meant that countries like Egypt, Jordan, and Pakistan were still accumulating fiscal pressure while European gas prices fell and the consensus relaxed. CDS spreads on these sovereigns are now structurally correlated to global ammonia prices. That correlation did not exist at this intensity before 2022.

The Euro itself has become something close to a petro-currency in reverse. Its valuation now tracks the energy trade balance more reliably than interest rate differentials. The standard model broke in 2022. It has not been repaired.

The Chain Is Structural

The Baltic Sea is not a regional waterway. It never was. For a brief window in the late 20th century, it was the artery through which cheap Russian molecules were converted into European industry, which was converted into global food production capacity. That window is closed.

The dependency it exposed — the conversion chain from hydrocarbon molecule to synthetic nitrogen to human calorie — did not close with it. That chain runs through every major energy chokepoint on the planet. The infrastructure changed in 2022. The vulnerability did not.

What remains is not crisis. Crisis implies a return. What remains is a new topology of risk, one that most policymakers are still mapping with the old charts, wondering why nothing quite lines up anymore.