The AI Capex Cycle Is Priced for Perfection. The Power Grid Isn't Ready.

Capital moves at the speed of conviction. Infrastructure moves at the speed of permits, pipelines, and political will. When these two timelines diverge far enough, the gap between them becomes a reckoning.

The Bet the Market Has Already Accepted

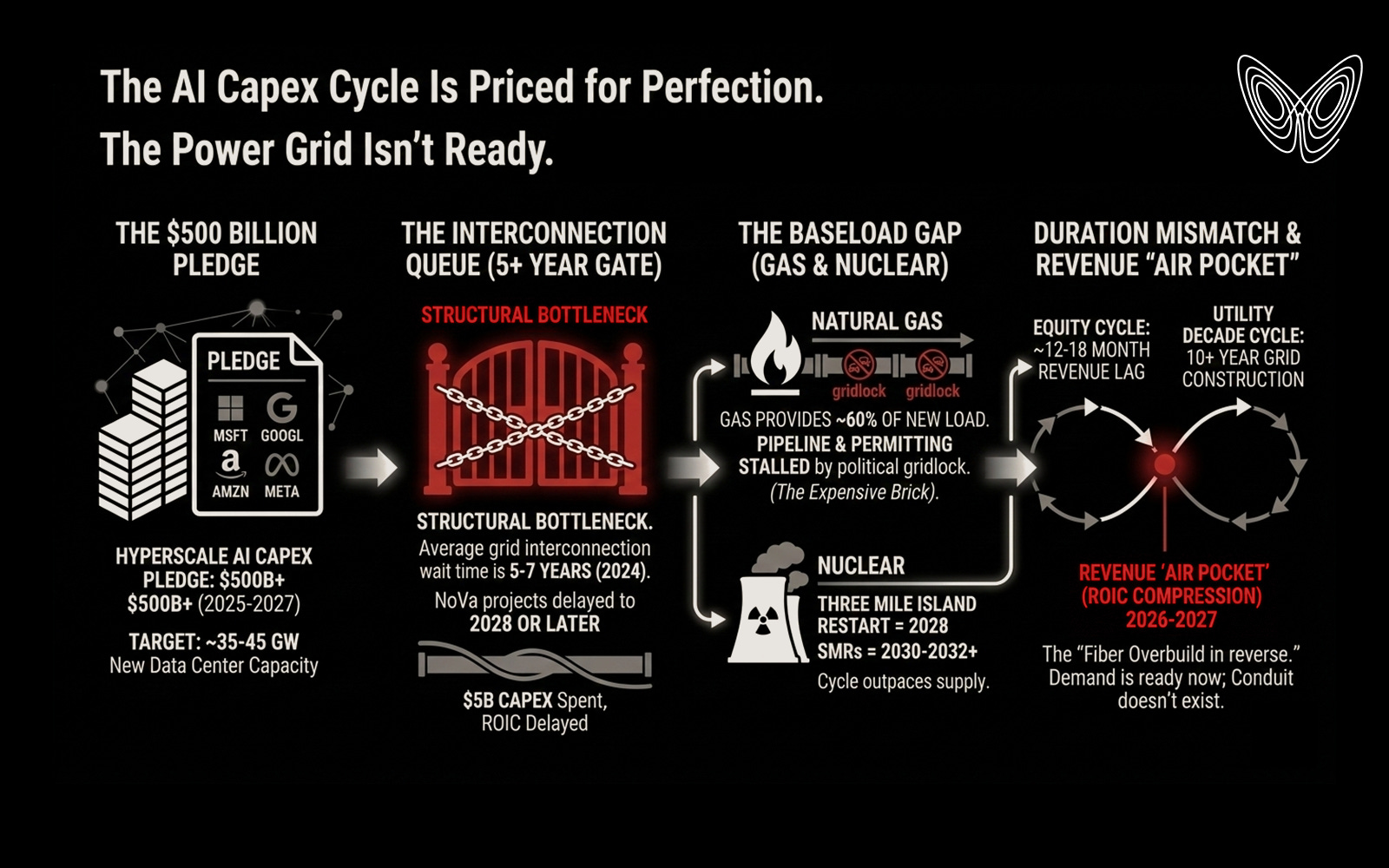

Microsoft, Alphabet, Amazon, and Meta have collectively announced CAPEX projections exceeding $500 billion for the 2025–2027 window. The thesis: AI compute demand is exponential, data center capacity must scale to meet it, and whoever builds fastest wins.

The equity market has accepted this thesis with a completeness that should itself be cause for suspicion. The NASDAQ-100 is pricing the compute. It is not pricing the conduit.

The NASDAQ-100 is pricing the compute. It is not pricing the conduit.

The Scale of the Problem

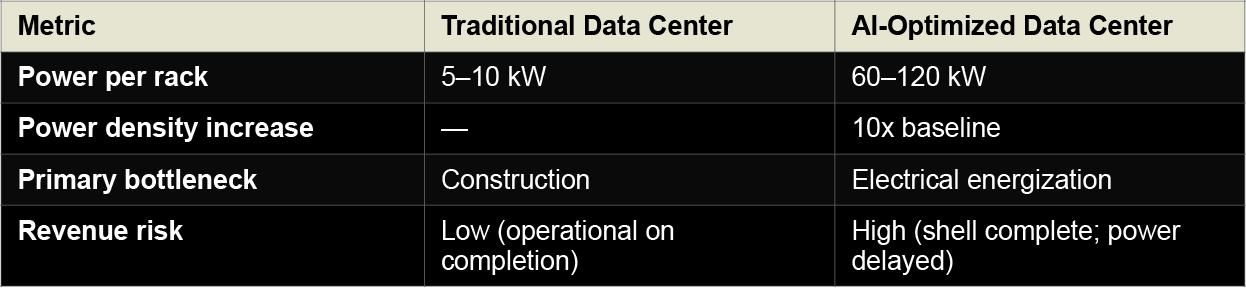

The industry is attempting to add between 35,000 and 45,000 megawatts of new data center capacity in North America by 2028. For reference, 1,000 megawatts is roughly the output of a large nuclear reactor. The sector is attempting to add the equivalent of 35 to 45 nuclear reactors' worth of power draw in under four years—into a grid not designed for this load, through a permitting system not built for this pace.

This is not a linear scaling challenge. A building that physically exists, has been constructed, and appears on a balance sheet as a capital asset, may still be unable to generate revenue because the electrical infrastructure required to bring it to life does not yet exist.

The shell is not the bottleneck. The energization is.

Where Equity Models Break

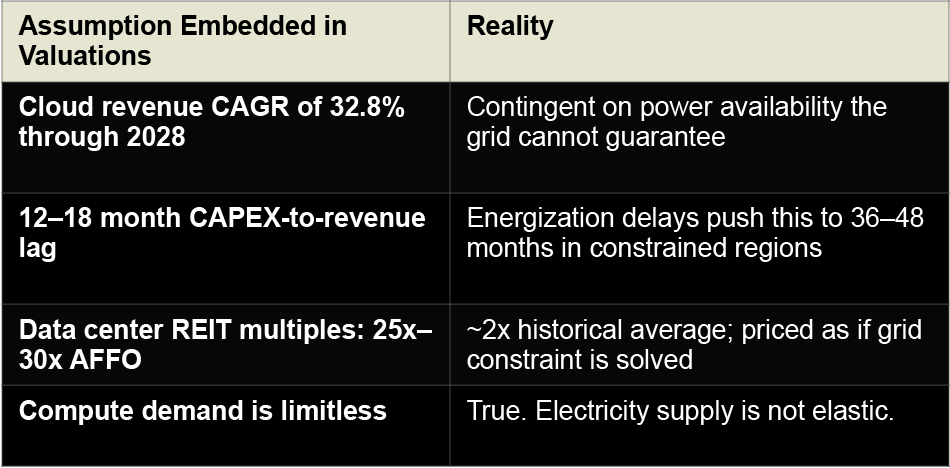

Equity consensus models for cloud service providers typically assume a 12 to 18 month lag between CAPEX deployment and revenue realization. Data center REITs are trading at 25x to 30x AFFO multiples—nearly double their 10-year historical average.

The demand for compute is priced as limitless. The supply of electricity is priced as elastic. Neither assumption survives contact with how a utility actually operates in the short and medium-run.

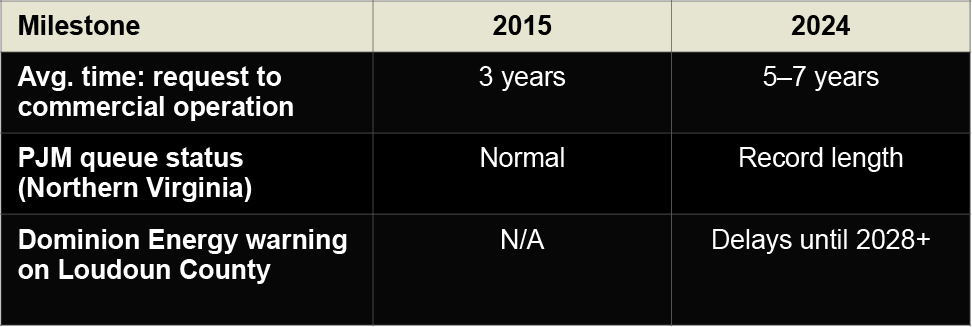

The Interconnection Queue: The Mechanism the Market Isn't Pricing

Before a data center can draw power, it requires an Interconnection Agreement from an Independent System Operator. This is not a formality.

A hyperscaler that commits $5 billion to a facility in 2025 and cannot draw full power until 2028 has created a non-productive asset that sits on the balance sheet without generating the revenue the valuation model assumed. The CAPEX is real. The return on that capital is deferred. The multiple does not reflect the deferral.

The Renewable Energy Framing Obscures a Simpler Problem

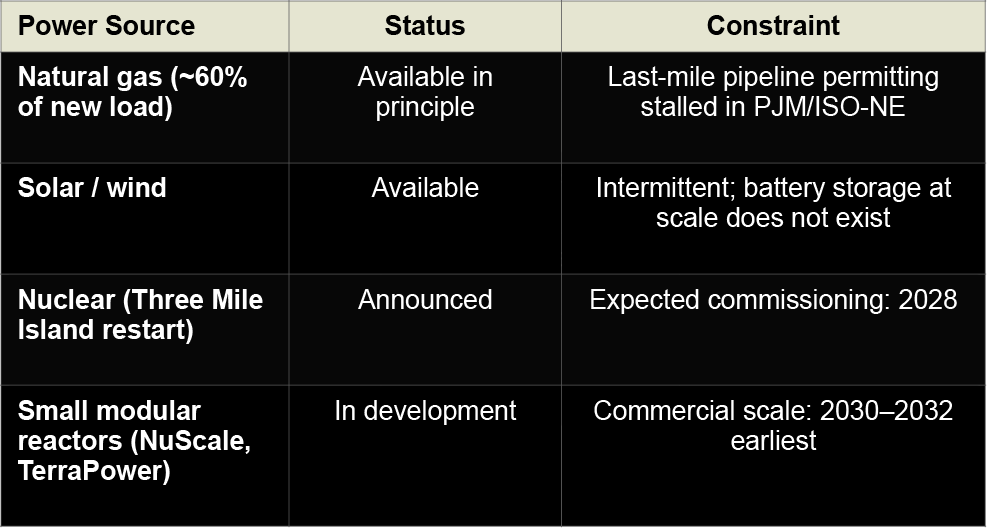

Hyperscalers promote 100% renewable targets. AI operations require continuous baseload power around the clock. Solar and wind are intermittent. The battery storage infrastructure required to bridge that intermittency at scale does not currently exist.

The Mountain Valley Pipeline required nearly a decade to clear its legal obstacles. New lateral pipelines to serve specific data center clusters face structurally similar opposition. Without the last-mile gas delivery, the facility cannot operate. The capital deployed to build it is stranded.

Nuclear is the forward solution. The timeline disqualifies it as a near-term answer. There is a three-to-five year window where AI CAPEX deployment will substantially outpace nuclear availability.

The Political Dimension Is Materializing

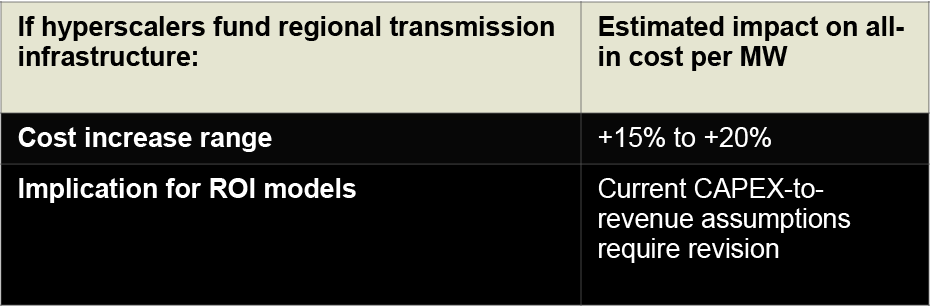

Dominion Energy's 2024 rate case filings indicated that residential customers in Virginia could see significant increases to fund more than $10 billion in transmission upgrades—a cost driven largely by data center growth.

Legislative efforts in Maryland and Virginia are advancing proposals to shift the cost of regional grid upgrades onto data center developers directly.

The social license to operate, which the sector has largely taken for granted, is becoming a negotiated commodity.

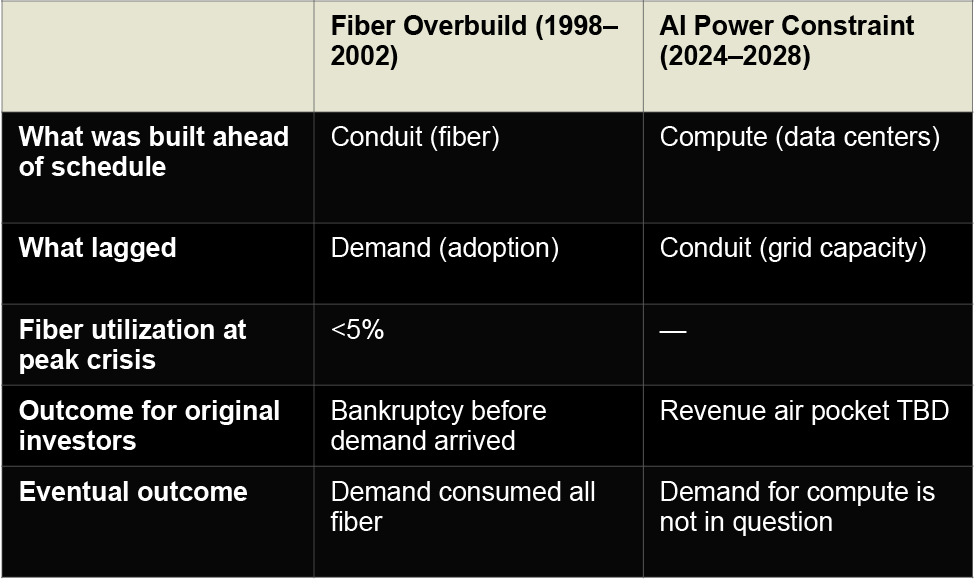

The Historical Analogue: The Fiber Overbuild (1998–2002)

Global Crossing, WorldCom, and their peers spent billions deploying trans-oceanic and long-haul fiber on the conviction that internet traffic was doubling every 100 days. The demand was genuine. The error was temporal.

In the fiber overbuild, the conduit was built and the demand was not yet there. In the current cycle, the demand is present and accelerating—but the conduit, the grid itself, does not yet exist at the required scale.

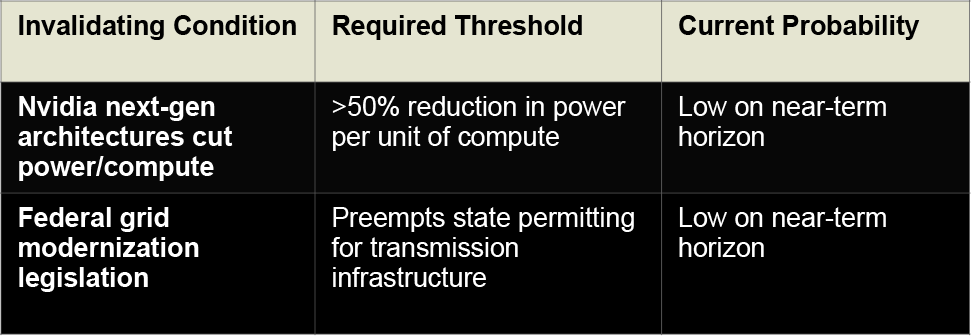

What Would Invalidate This Thesis

Two conditions would change the analysis materially:

In the absence of either outcome, what remains is a duration mismatch of unusual severity. Equity markets operate on quarterly and annual cycles. Utility infrastructure operates on decade-long ones.

The Shockpath

The PP&E will accumulate on hyperscaler balance sheets. The revenue from unlit, under-powered facilities will not arrive on the schedule the models assume. The result is not a demand collapse—demand for AI compute is not in question.

The result is a revenue air pocket in 2026 and 2027 that will force the market to reprice the efficiency of the capital being deployed.

The grid does not know what a roadmap is. It does not respond to earnings calls or analyst days. It operates on the physics of permitting, construction, and interconnection—timelines that were old before the word 'hyperscale' existed.

The capital has moved. The infrastructure has not. That distance is the shockpath.