The $3.5 Trillion Homecoming: Japan's Yield Curve Exit and the Global Rate Shockpath

Every system built on distortion eventually corrects. The question is never whether. It is when, and how violently.

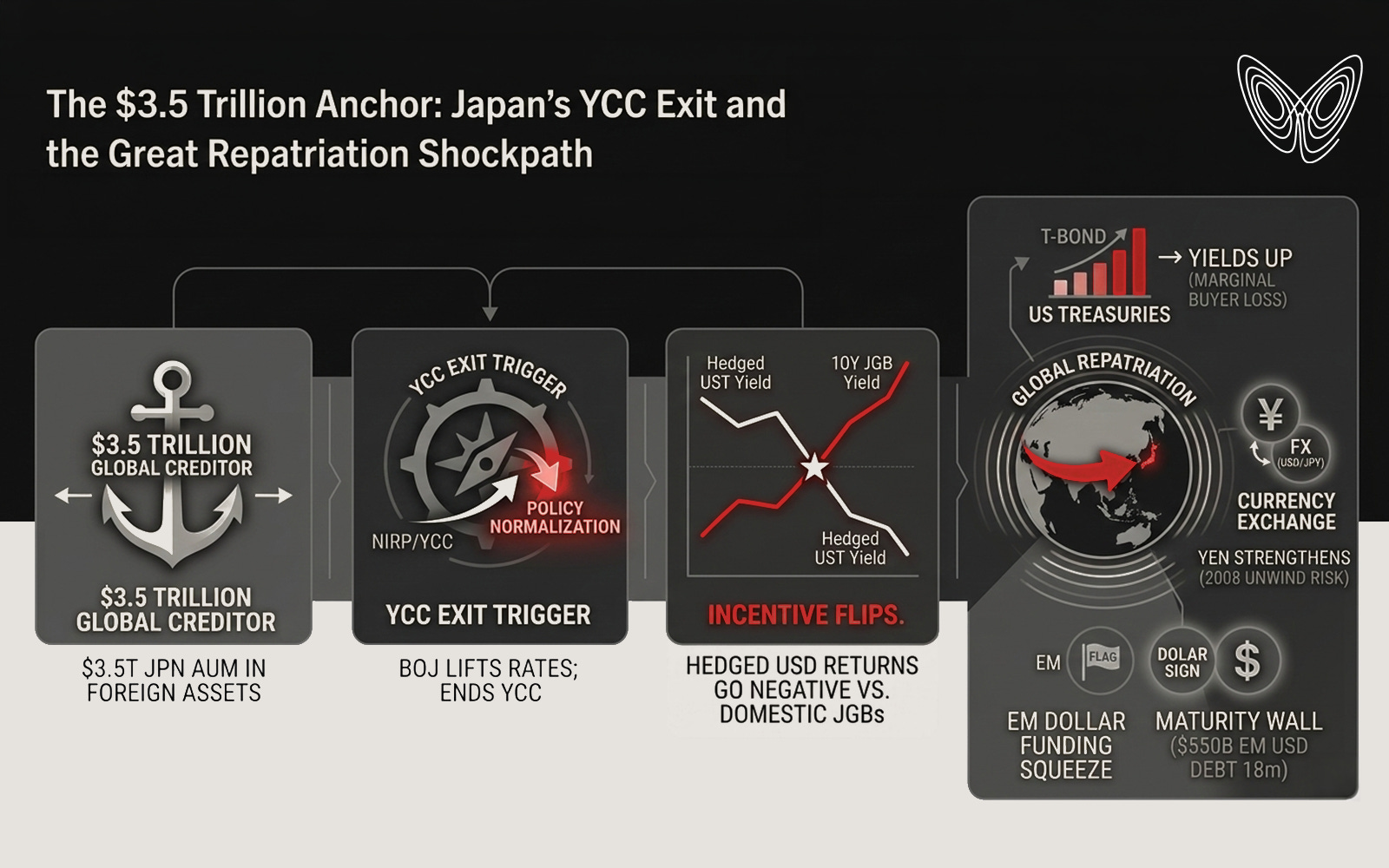

For two decades, the Bank of Japan held domestic yields near zero and forced the world's most disciplined institutional capital into a relentless search for yield abroad. That capital found its way into US Treasuries, European sovereign debt, and the funding corridors of emerging markets. Roughly $3.5 trillion of it, by most estimates. The mechanism was simple: Japanese yields offered nothing, so Japanese money left.

It is now beginning to return.

The pivot began quietly on December 20, 2022, when Governor Kuroda widened the 10-year JGB yield target band from ±0.25% to ±0.50%. Markets called it a technical adjustment. By July 2023 the effective ceiling had moved to 1.0%. By March 2024, Yield Curve Control was officially abolished and negative interest rates ended. By July 2024, the policy rate was at 0.25% with active reductions in monthly JGB purchases. As of early 2026, the rate sits at 0.50%, with overnight swaps pricing a 68% probability of another 25-basis-point hike at the April 28th meeting and a terminal rate near 1.0% by year-end.

The consensus reads this as choreographed. USD/JPY has retraced from its 2024 peak near 161.95 to the 140 to 145 range. Implied volatility in 1-month options has fallen from 12.5% to 9.2%. Markets are calm. Markets are also wrong about what they are measuring.

The Overlooked Mechanism

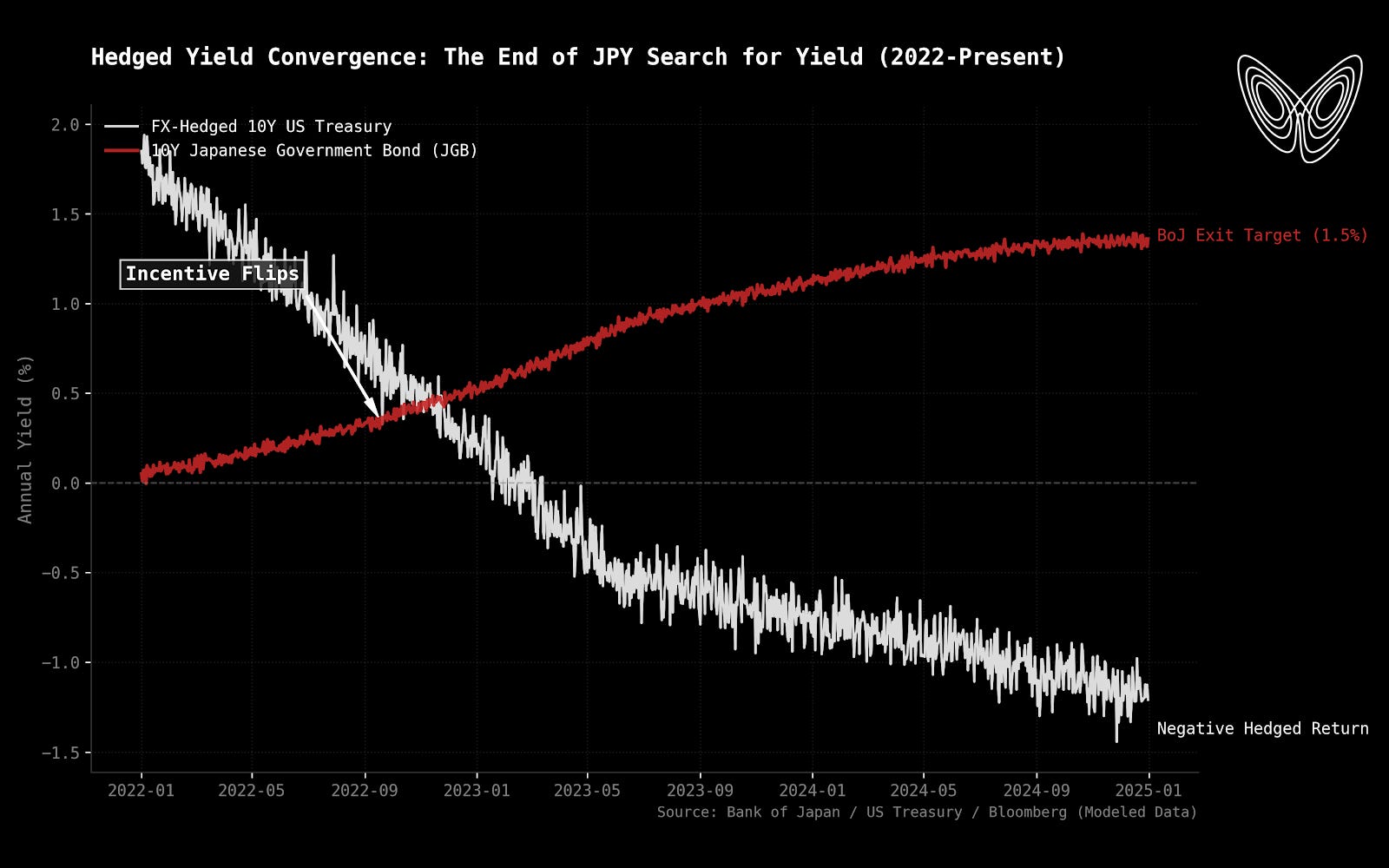

The consensus treats this as a domestic Japanese event. It is not. It is a global fixed-income event dressed in domestic clothing. And the mechanism that most participants are not tracing is the FX-hedged yield, not the nominal one.

A Japanese life insurer holding a 10-year US Treasury does not care about the coupon in isolation. What matters is what remains after hedging the dollar exposure back to yen. With the USD/JPY 3-month basis swap reflecting elevated US short-term rates, that hedging cost has hovered between 4.5% and 5%. Against a 10-year Treasury yielding 4.2%, the math produces a negative hedged yield for a Japanese buyer. Meanwhile, the 10-year JGB is now approaching 1.5%, a level consistent with the historical hurdle rate Japanese insurers require on their liability books.

When home yields reach parity with the hedged foreign alternative, the structural incentive to hold foreign assets collapses. This is not a sentiment shift. It is arithmetic.

The Flow Math

The numbers beneath that arithmetic are significant. GPIF, the world's largest pension fund, holds approximately ¥60 trillion in foreign bonds. Japan Post Bank and the major life insurers collectively hold over $1.1 trillion in foreign fixed income. Total foreign bond holdings by Japanese residents stand near $3.5 trillion. Approximately $1.1 trillion of that sits in US Treasuries, representing roughly 14% of all foreign-held US debt.

A 10% repatriation of those US Treasury holdings over 12 months means roughly $9.1 billion in monthly selling pressure. The average monthly 10-year Treasury auction size is $40 to $42 billion.

That is nearly a 22% increase in effective supply to a market that primary dealers are already stretched to absorb. Yields do not drift higher in that scenario. They are pushed.

The Periphery Pays First

A rising US 10-year yield does not occur in isolation. It raises the floor for all dollar-denominated debt. And when global liquidity contracts as the world's largest creditor withdraws from external markets, risk premiums widen.

Emerging market sovereigns are carrying approximately $550 billion in dollar-denominated debt maturing within the next 18 months. Turkey, Egypt, and Colombia — all operating with thin reserve buffers and high external financing requirements — face a refinancing shock if the US 10-year is trading toward 5% under Japanese selling pressure.

These are not hypothetical casualties. They are the predictable periphery of a structural flow event.

European sovereign debt carries a quieter exposure. Japanese insurers hold significant positions in French OATs and Belgian government bonds, estimated at over €200 billion combined. These holdings represent a meaningful share of foreign ownership in markets that have relied on price-insensitive Japanese demand for years. When that demand rotates home, the bid that European treasuries have taken for granted does not get replaced automatically. It gets repriced.

What Rhymes But Does Not Repeat

The 2011 Tohoku earthquake offers the closest historical analogy. Anticipating insurer repatriation to cover domestic claims, USD/JPY fell from 83.00 to 76.25 in five days. The move was severe enough to trigger a rare G7 coordinated intervention on March 18, 2011.

That episode involved perceived necessity, not mathematical certainty. What is building now has a different quality. The hedged-yield pivot is structural, not event-driven. It does not require a catalyst. It requires only time and arithmetic to run its course.

The current volatility pricing in US Treasury options reflects a Fed-driven narrative. It does not reflect the possibility of a supply-side shock originating from the world's largest creditor.

That gap between implied and actual risk is where the asymmetry lives.

What Suppresses It, And What Doesn't

Two scenarios could slow the move. A rapid US rate-cut cycle collapsing hedging costs back to levels that restore the relative attraction of Treasuries. Or a Ministry of Finance intervention, formal or informal, to slow the pace of repatriation and prevent excessive yen strengthening.

Both are possible. Neither is the base case.

What is the base case is a slow, institutional, mathematically-driven withdrawal of the largest source of external demand the US Treasury market has ever known. Not a crisis. Not a panic. Something more difficult to trade: a structural tide going out, one that most participants will not identify until the waterline is already lower than it was.

The global fixed-income architecture of the last two decades was built on the assumption that Japanese capital would always need somewhere else to go. That assumption held while domestic yields offered nothing. It is no longer holding. And the infrastructure that was built on top of it — the EM funding corridors, the European sovereign bid, the Treasury auction mechanics calibrated for reliable foreign demand — does not adapt gracefully to the removal of its foundation.

It adapts the way all systems built on distortion adapt. Late, and all at once.