Strait of Hormuz: $20 Billion Against $352 Billion

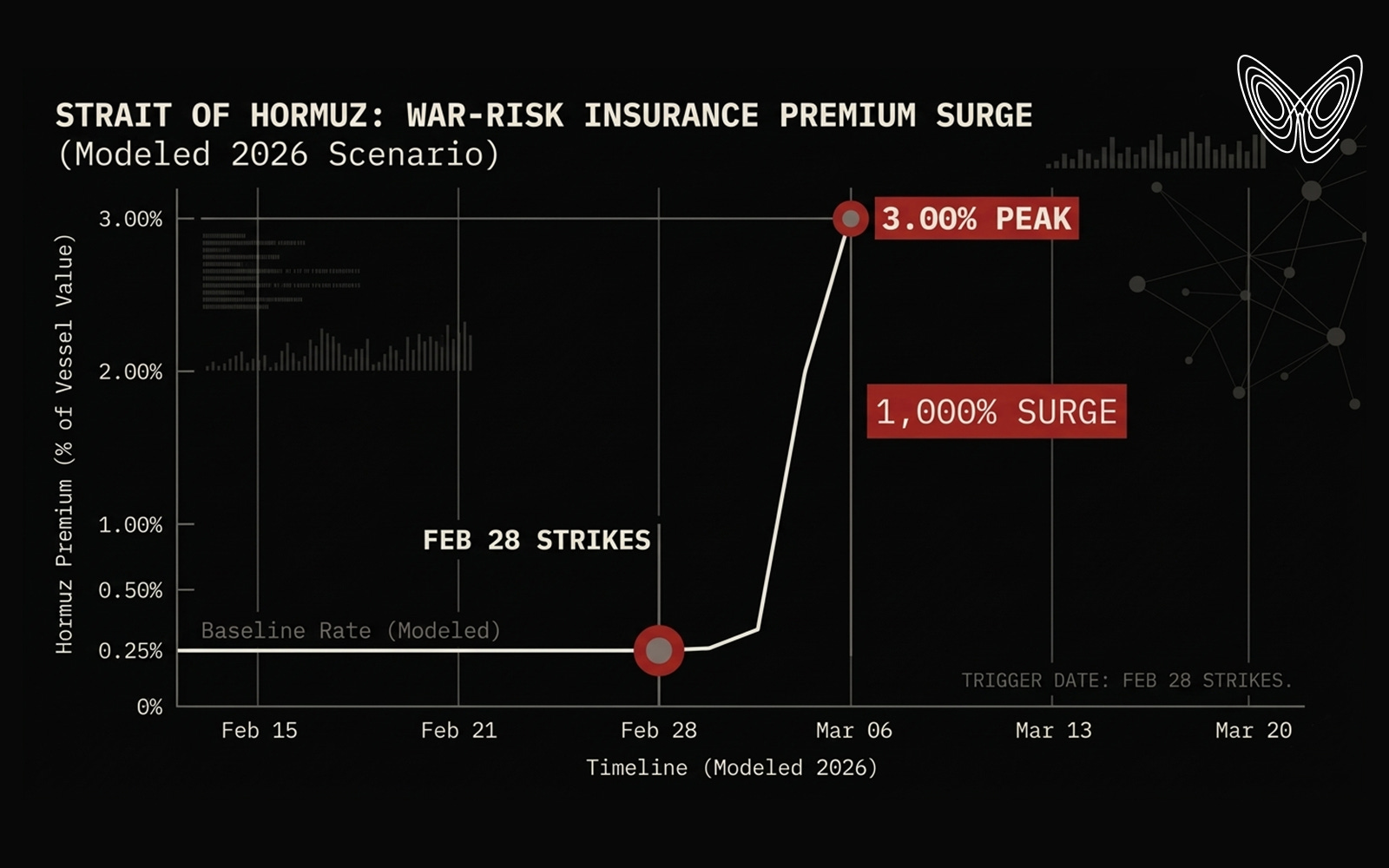

War-risk insurance premiums on Strait of Hormuz transit just moved 1,000%. Not 10%. Not 50%. A thousand percent. From 0.25% of vessel value to 3% by March 6, 2026.

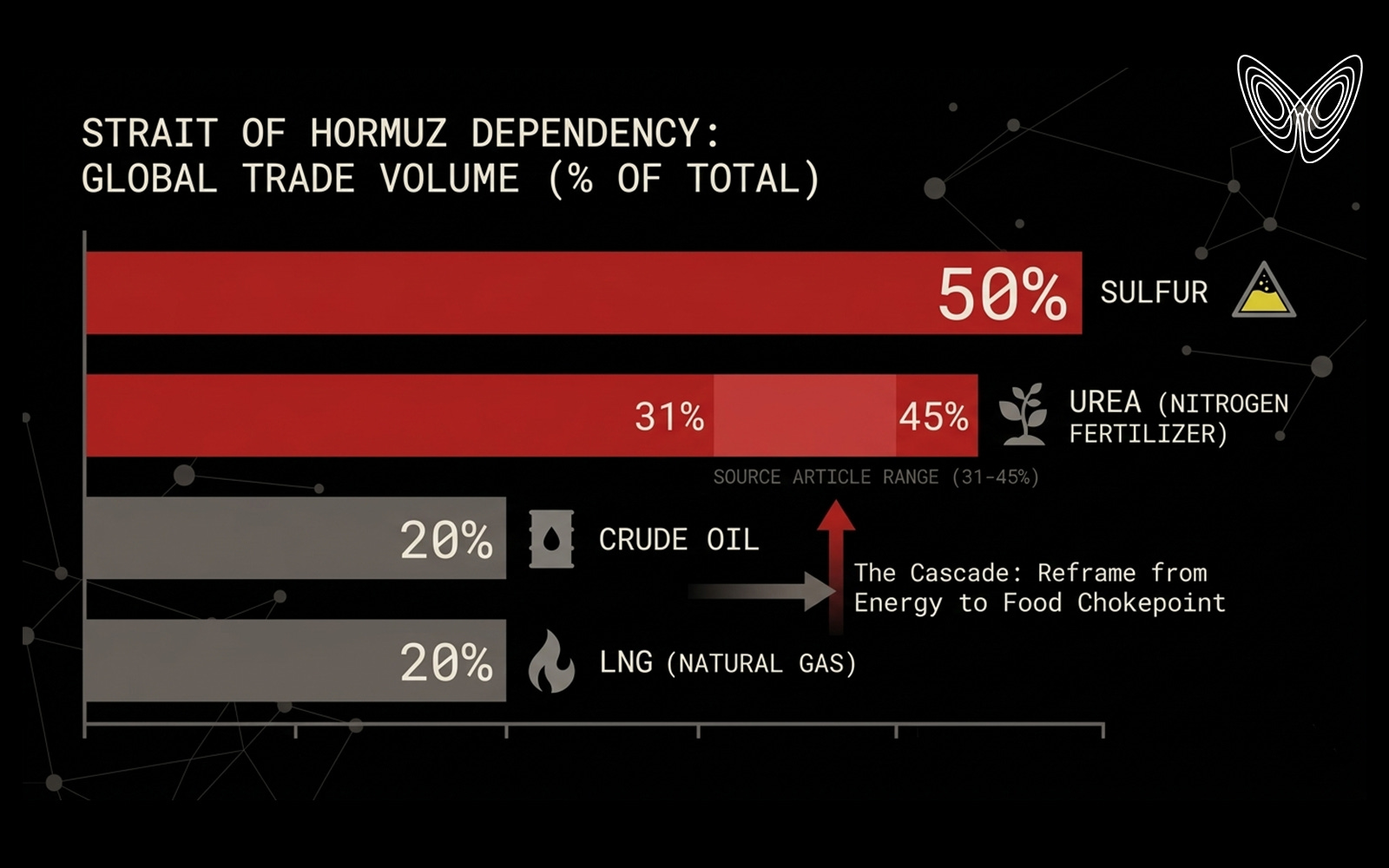

Nearly 50% of the world's traded sulfur. Between 31% and 45% of global urea shipments.

Not because it signals danger — the market already absorbed the kinetic escalation narrative when U.S. and Israeli strikes hit Tehran leadership compounds on February 28. The market priced a war. It has not priced what the insurance industry did in response.

Those are two entirely different trades.

The First-Order Story

The headline read: U.S.-Israel strikes on Iran. Oil surged. Brent jumped nearly 30%, touching $116 a barrel in Asian trading. Goldman Sachs warned that a sustained crisis could push prices past their 2008 and 2022 peaks — above $147 and $5/gallon gasoline respectively. The implied volatility curve in crude options steepened sharply at the front end.

Consensus interpretation: temporary supply disruption. Elevated geopolitical risk premium. Four-week closure scenario. Strategic reserves as the release valve.

The 30-day implied vol is running 17.5 points wide of the 90-day. The market is paying enormous premium for near-term protection and simultaneously betting that the structural situation normalizes within a quarter.

That is a mispricing with a very specific mechanism attached to it.

The Paperwork Closed It

The Strait of Hormuz is not closed because of missiles. It is closed because of paperwork.

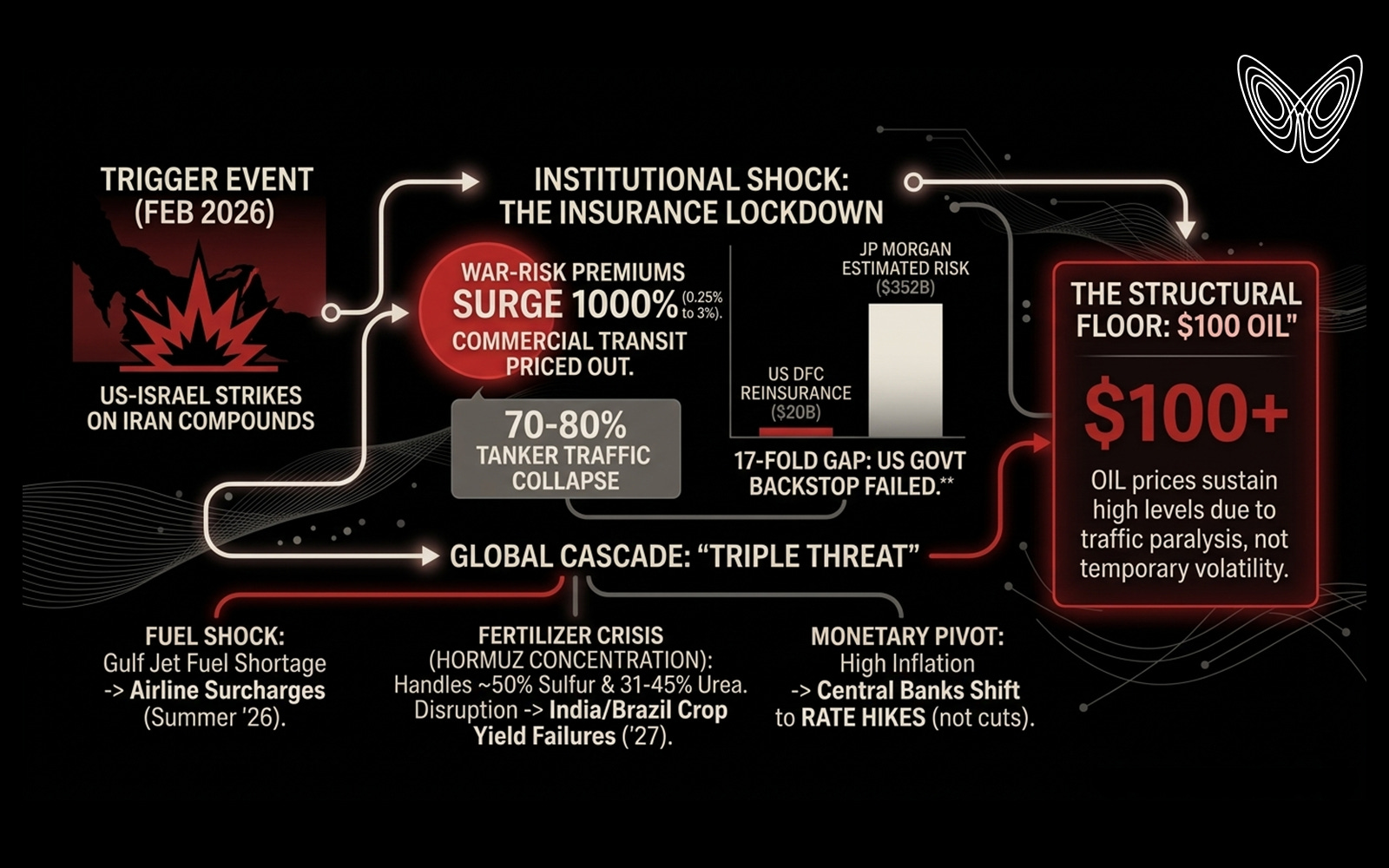

On February 28, after the strikes, the Protection & Indemnity clubs — the mutual insurers that provide the liability backbone of global shipping, institutions like Gard and Skuld operating out of London and Oslo — issued Notices of Cancellation on war-risk cover for Gulf transit. These are not requests. They are contractual cancellations with 7-day notice periods. They are non-poolable, meaning no reinsurance syndicate will absorb this risk at any commercially viable price. The clubs made a structural determination, not a reactive one.

The result: 70-80% collapse in tanker traffic transiting the Strait.

The physical closure didn't require a minefield. It required a policy endorsement withdrawal.

Ships that attempt transit without commercial insurance void their hull policies entirely. Shipowners accepting DFC-backed government coverage must follow Navy-approved transit corridors — corridors that, if breached, cancel the remaining excess policies and create a single point of failure for the entire fleet operation. The U.S. Navy currently has 12 warships in the Middle East theater, most already committed to active strike operations and missile intercept. Continuous dedicated escort for hundreds of tankers is not a logistics challenge. It is a logistics impossibility without a full redeployment of global naval assets.

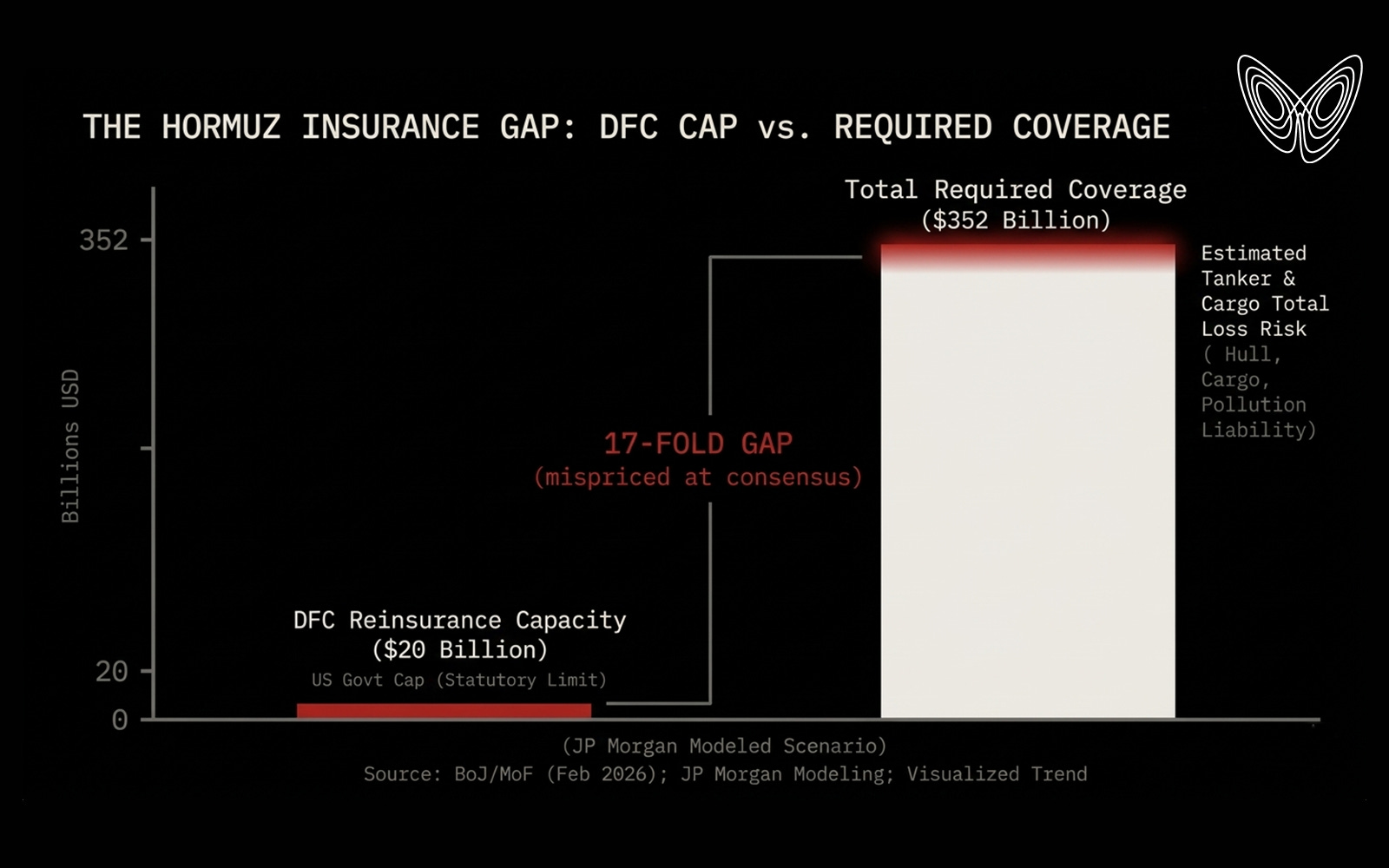

This is why the Trump administration's announcement of $20 billion in DFC political risk reinsurance is not a backstop. It is a rounding error.

J.P. Morgan estimates total loss coverage for the 329 oil tankers and container ships currently trapped in the Gulf at $352 billion. The DFC statutory limit is $205 billion. Current headroom: $154 billion. The gap between announced intervention and required coverage: $332 billion, a 17-fold shortfall.

The market is treating a $20 billion announcement as a sovereign backstop against a $352 billion exposure. That spread between consensus and reality just widened.

The Dependency That Cannot Be Rerouted

Modern industrial agriculture is not a biological process. It is an energy conversion process. Natural gas becomes ammonia through the Haber-Bosch reaction. Ammonia becomes urea. Urea becomes nitrogen fertilizer. Nitrogen fertilizer becomes calories. The Strait of Hormuz handles 20% of global LNG — which means the single most important node for global food security and the single most important node for global energy transit are the same chokepoint.

The Cape of Good Hope reroute adds 10-14 days to voyage time and works reasonably well for crude oil. It does not solve fertilizer logistics. Urea degrades in storage. Sulfur shipment windows align with agricultural planting cycles. The 2027 planting cycle in India and Brazil depends on input deliveries that have a hard calendar constraint. Ships stuck in a Cape routing pattern, with 14 extra days of voyage time and surge freight costs, cannot simply make up for lost time at the margin.

That is not a supply disruption. That is a yield failure already in progress — it just won't show up in consumer food prices until 2027.

The Haber-Bosch node is where this shockpath crosses from an energy crisis into a food security emergency. It is the structural pivot in this chain. It is the link that makes this story matter to people who have no portfolio exposure to energy futures.

Six Links. Four Continents.

U.S.-Israel strikes on Tehran leadership compounds → P&I club war-risk cancellations (London, Oslo, Singapore) → 70-80% tanker traffic collapse and Cape rerouting → Gulf jet fuel and urea/ammonia feedstock shortages → European airline surcharge spikes (summer 2026) and 2027 crop yield failures in India and Brazil → consumer food price emergency that arrives 12 months after the insurance story closes.

Six links. Four continents. The cascade started. Most people are watching link one.

The terminal consumer exposure — summer airfares, grocery prices in 2027 — is not a secondary effect. It is the mechanism through which an institutional story about P&I clubs in Oslo becomes a political crisis for governments in New Delhi, Brasília, and Berlin.

The 1980 Echo

The nearest historical precedent is the 1980-1988 Tanker War, when Iraq and Iran systematically targeted commercial shipping in the Gulf. The U.S. response — reflagging Kuwaiti tankers and providing naval escorts — is structurally analogous to what the DFC/Navy combination is attempting today.

The critical difference: in the 1980s, the U.S. reflagging occurred before the insurance market had fully repriced. The institutional withdrawal was less complete. And the agricultural input dependency through the Strait was meaningfully lower — the scale of Gulf petrochemical export into the global fertilizer supply chain has grown substantially in four decades.

The 1980 trigger produced a U.S. recession beginning in July 1981, an eight-month lag from supply shock to business cycle peak. The mechanism in 2026 is faster in some channels (real-time freight repricing, instant insurance cancellation) and slower in others (the agricultural cycle that won't register until 2027 planting fails).

The precedent confirms the mechanism. It does not confirm the timeline or the magnitude. 2026 has higher global food system concentration, more complete insurance institutional withdrawal, and a U.S. Navy with fewer available assets relative to the escort requirement.

The Dates That Cannot Deliver

The April 5, 2026, OPEC+ monitoring group meeting — Saudi Arabia, Russia, Iraq, UAE, Kuwait, Kazakhstan, Algeria, Oman — is the first forced decision point. These eight countries must determine whether to accelerate production to offset the 70-80% tanker traffic collapse.

The constraint: accelerating production means nothing if the physical export flows cannot transit. OPEC+ spare capacity is not the binding variable. Insurance capacity is. A production decision made on April 5 that cannot be physically exported does not close the gap.

The June 7 full OPEC+ ministerial meeting is the subsequent window for 2027 baseline renegotiation — decisions that will be made in the context of a Strait that has been structurally impaired for over three months by that point.

Neither date resolves the insurance lockdown. They are resolution windows for downstream decisions that depend on a prior condition — commercial transit viability — that neither OPEC+ nor the DFC controls.

The market is pricing resolution at the April 5 meeting. The April 5 meeting cannot produce resolution. The binding constraint is in the P&I clubs' actuarial models, not the OPEC+ communiqué.

Where the Mispricing Lives

The crude oil market has priced a four-week disruption with substantial near-term vol premium. The agricultural input market has priced almost none of the sulfur and urea disruption. The aviation market has partially priced summer fuel costs but not the structural duration.

The $332 billion insurance gap does not close in four weeks. It closes when the London market reassesses the war-risk environment — which is a function of the kinetic situation on the ground, the credibility of the DFC backstop, and the Navy's demonstrated ability to provide continuous escort. None of those conditions are on a four-week timeline.

What rhymes with this in the historical record: the 1973 oil embargo produced price effects that lasted years, not weeks, because the institutional repricing that accompanied it was structural. Prices did not return to pre-crisis levels until the institutional environment changed, not the kinetic one.

A $100 floor on crude is not a prediction. It is the arithmetic of a 70-80% traffic collapse sustained for longer than four weeks when the only relief valve is a government program with $154 billion in headroom against $352 billion in required coverage.

The more interesting asymmetry is in fertilizer inputs, where current pricing reflects essentially no disruption premium. If the Strait remains non-viable for commercial transit through the April planting preparation cycle, the 2027 crop yield impact in India and Brazil is not a tail risk. It is the base case.

That is not a headline. That is a structural rupture in global nitrogen supply.

The fault line here is not in the oil market, where everyone is already positioned. It is in the agricultural input chain, where the transmission lag means the damage will not be visible until long after the narrative has moved on to whatever comes next.